Housing & Dreams Delayed

With more than 2.8 million COVID-19 cases, Texas has the second highest total number of cases in the U.S. and the communities in the state’s Rio Grande Valley (RGV) have been hit particularly hard. The largely Latino population living in the RGV has experienced a staggeringly high number of COVID-19 fatalities per capita that puts into undeniable terms the disproportionate effects of the COVID-19 pandemic on low-income communities of color. The subsequent economic downturn has affected the region unevenly – creating a boom for some and a bust for others. At one end of the spectrum, low-wage earners considered essential who remained healthy have seen their incomes rise as their work hours increased, enabling some to save money during this period. At the other end, low-wage earners in sectors severely harmed by the pandemic and local restrictions have struggled to pay their bills when parts of the economy shut down and unemployment benefits expired.

As housing counselors at the Brownsville, TX-based non-profit “Come Dream. Come Build” (CDCB) can attest, the pandemic has upended the lives of many of their clients like Elena Sanchez, hampering the dream of homeownership. These are the some of the tough housing challenges Fannie Mae seeks to address in partnership with organizations like CDCB to help ensure that dreams delayed are not denied.

Come Dream. Come Build. – Turning Low-Income Residents into Homeowners

The pandemic layered on another strain for low-income people in high-needs, underserved markets wanting to buy a home. This was the case for Elena Sanchez of Brownsville who always knew she wanted to own a home. In fact, she and her husband began building a house in Mexico before moving to the U.S. nearly eight years ago. Initially, they lived with their two sons in a single room. They later moved into a trailer, giving them more space, but Elena knew it was not a suitable home for her family which had grown to five people after welcoming a baby girl. “I knew I would not be at peace until after I purchased a home of my own,” Elena says.

When Elena’s sister purchased a home, she urged Elena to contact the organization that helped her, CDCB, a local mainstay in community development for 47 years. Elena eventually enrolled in CDCB’s housing counseling program in 2019 and was laser-focused on buying a home, but her plans were thrown into question when the pandemic struck.

Low-income residents in underserved markets like Elena who aspire to become homeowners often face significant challenges navigating the home purchase process, and the pandemic has made things that much harder. Organizations like CDCB provide much-needed assistance to residents across the RGV. Through their high-touch, one-on-one housing counseling program, CDCB staff develop empathetic relationships with clients as they build their financial capabilities and prepare them to realize their dream of homeownership.

When their offices closed last March, the CDCB team quickly reimagined the delivery of their core business services in a virtual setting. The transition to a technology-based environment was not easy for clients like Elena who had become accustomed to meeting with her CDCB counselor in person. “I had to learn to embrace technology to continue working toward my goal,” she says.

Other near-term effects of the pandemic – government office closures, construction site restrictions and supply chain disruptions – meant construction of Elena’s home was going to take longer than planned. The delayed schedule forced the family of five to continue living in their trailer. This became increasingly difficult with schools and daycares closed, keeping her kids ages 17, 14 and 4 at home all day while she and her husband went to work.

Frustrated by months of delays and anxious to move, Elena knew she could not let the setbacks deter her. She recalls saying to her children, “The day we move from this trailer will be because we are moving to a house that’s ours. And that’s what we did.” After a nearly six-month delay, the family finally moved into their new home in February 2021. Elena is proud of what she has accomplished. “It’s not a big house or a fancy house, but it is my house.”

Now we have stability. No more moving around, renting this place or that, or living with relatives. I have no plans to move from here. My husband and I will grow old together in this house.

help

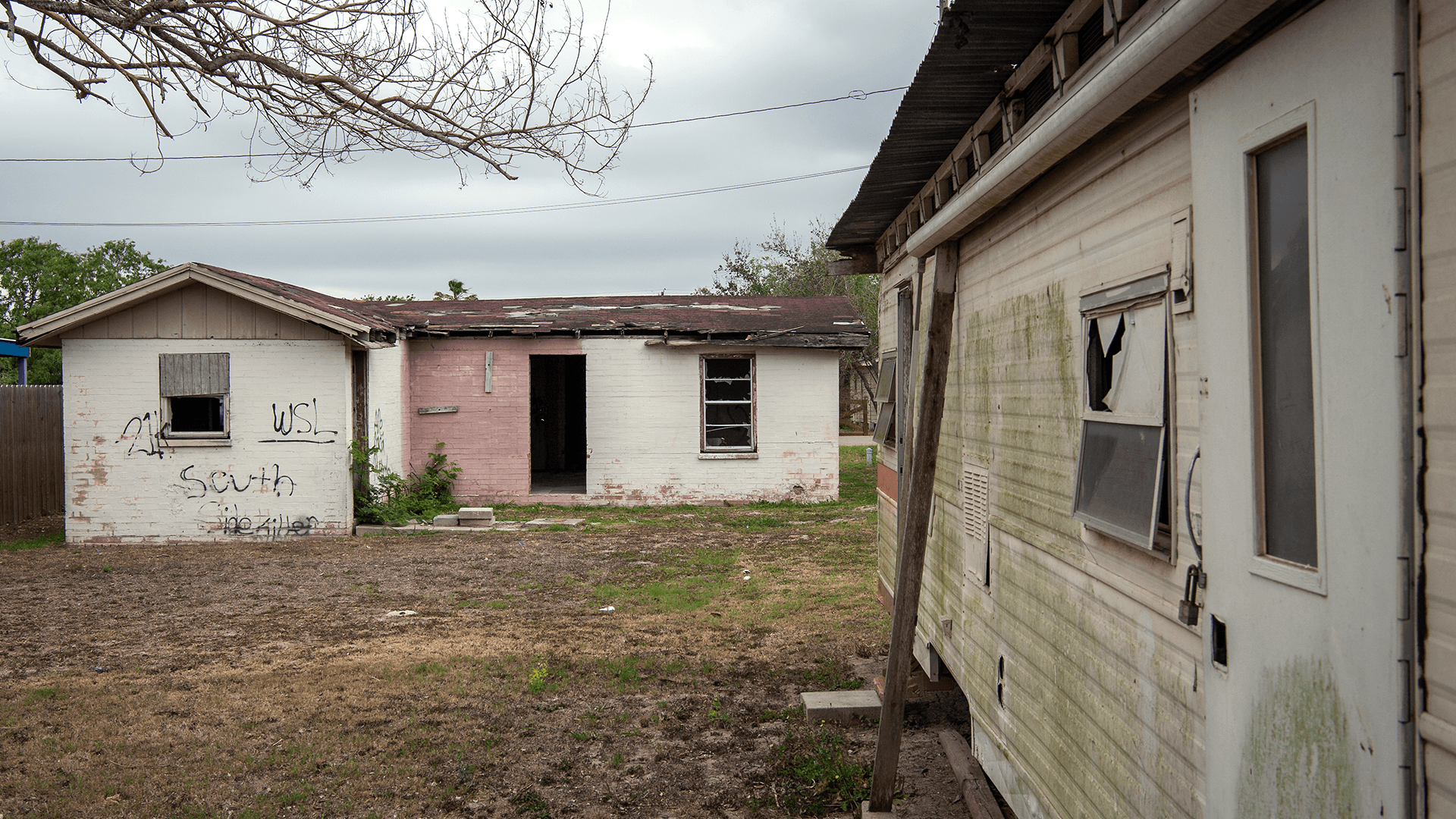

Elena’s story illustrates the many challenges families across the Rio Grande Valley face when trying to secure safe, stable housing. The stark issues of crowded living spaces, no access to electricity, or inadequate water and sewer systems that have defined the region for decades have only intensified during the pandemic.

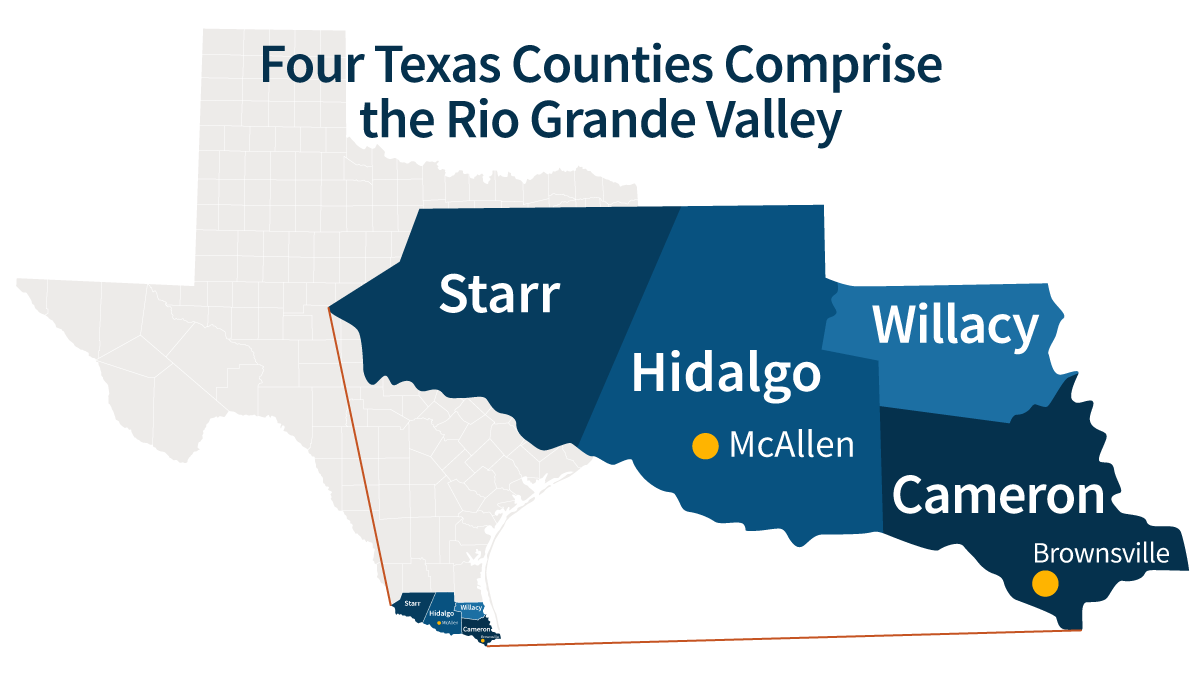

The four Texas counties that comprise the RGV – Hidalgo, Cameron, Starr, and Willacy – have a combined population of approximately 1.4 million. Approximately 93% of the population is Latino and just over 20% of residents were born outside of the U.S. The median household income is one of the lowest in the state at $36,000. Among the most impoverished areas in the country, the percentage of people living in poverty in each county of the RGV is higher than both the U.S. and Texas rates.

*Numbers are approximate.

The largest regional cities of McAllen and Brownsville are surrounded by colonias – small, unincorporated, often rural communities found along the U.S.-Mexico border that are typically characterized by the basic infrastructure they lack, such as potable water, sewer systems, electricity, paved roads, and safe housing. There are more than 2,450 colonias of varying sizes and densities in California, Arizona, New Mexico, and Texas. Given its long stretch of border with Mexico, it’s not surprising that Texas has the highest concentration of colonias, most of which are in the lower Rio Grande Valley.

Most experts agree that colonias initially formed in response to a lack of affordable housing. In Texas, colonias date back to the 1950s when developers took worthless farmland and divided it into small plots, which were then sold to low-income families who built homes in these unincorporated areas outside city limits. Promises that basic public services would soon come to the growing community were never fulfilled in most cases and the effects of this history endure to this day. According to a 2015 report from the Federal Reserve Bank of Dallas, despite significant investment over the years, approximately 38,000 residents still lack access to infrastructure commonly found in residential areas.

The need for affordable housing, the most salient driver in the formation of colonias, remains prevalent.

Gloria Palacios, another CDCB client, worked for most of her life as a migrant farmworker picking fruits and vegetables in different states alongside her husband. Now retired, the goal of homeownership has only gained importance for the soon-to-be first-time grandparents.

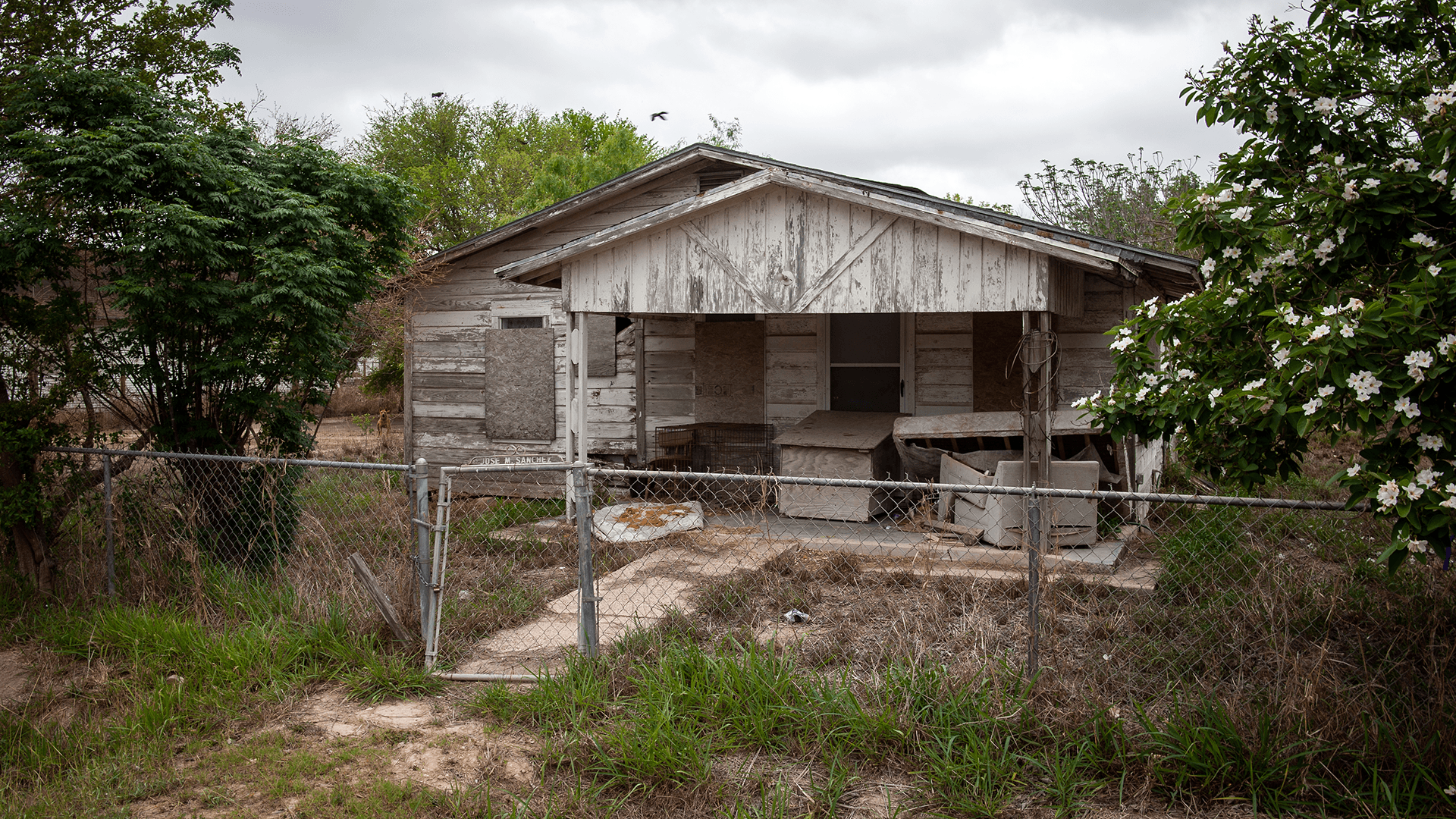

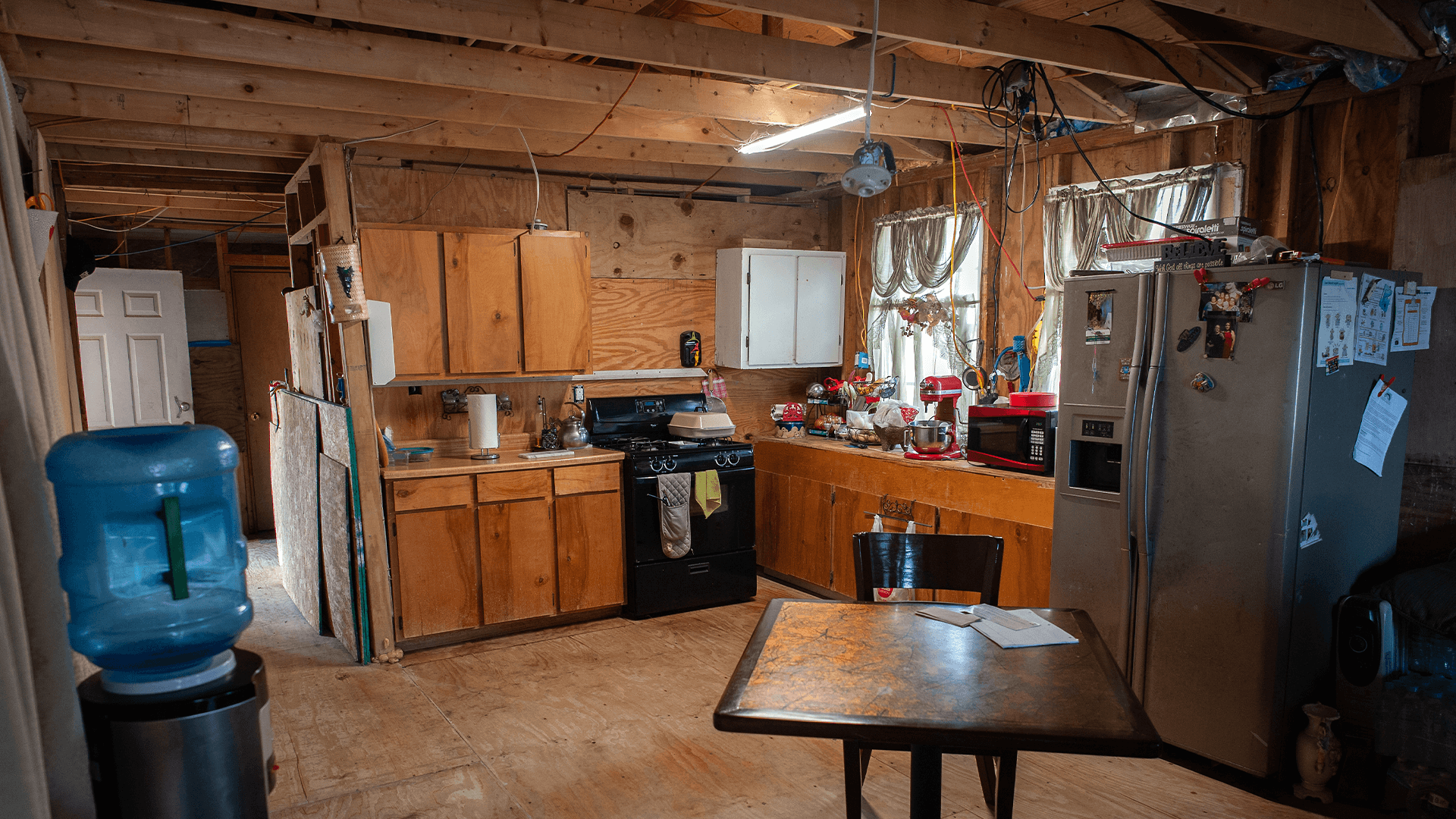

My house now is just four exterior walls. We don’t have insulation. We don’t have sheet rock. There’s no electricity in the bedrooms. We are older people, so we want a small house that supports aging in place.

Gloria describes the home she and her husband share with her 92-year-old mother-in-law as unsafe. They bought the Brownsville property years ago and have tried to fix up the dilapidated house over time. Despite the repairs, the house never passed the city inspection and so continuing to invest in it has become economically impracticable. Gloria’s daughter Erika recognizes that her parents’ current living situation is not conducive to complying with stay-at-home orders, which is why she supports her parents working with CDCB to buy a home. During the four years that Gloria has participated in the housing counseling program, she has made impressive strides – establishing a credit profile, significantly raising her credit score, maintaining a budget, and saving for a down payment.

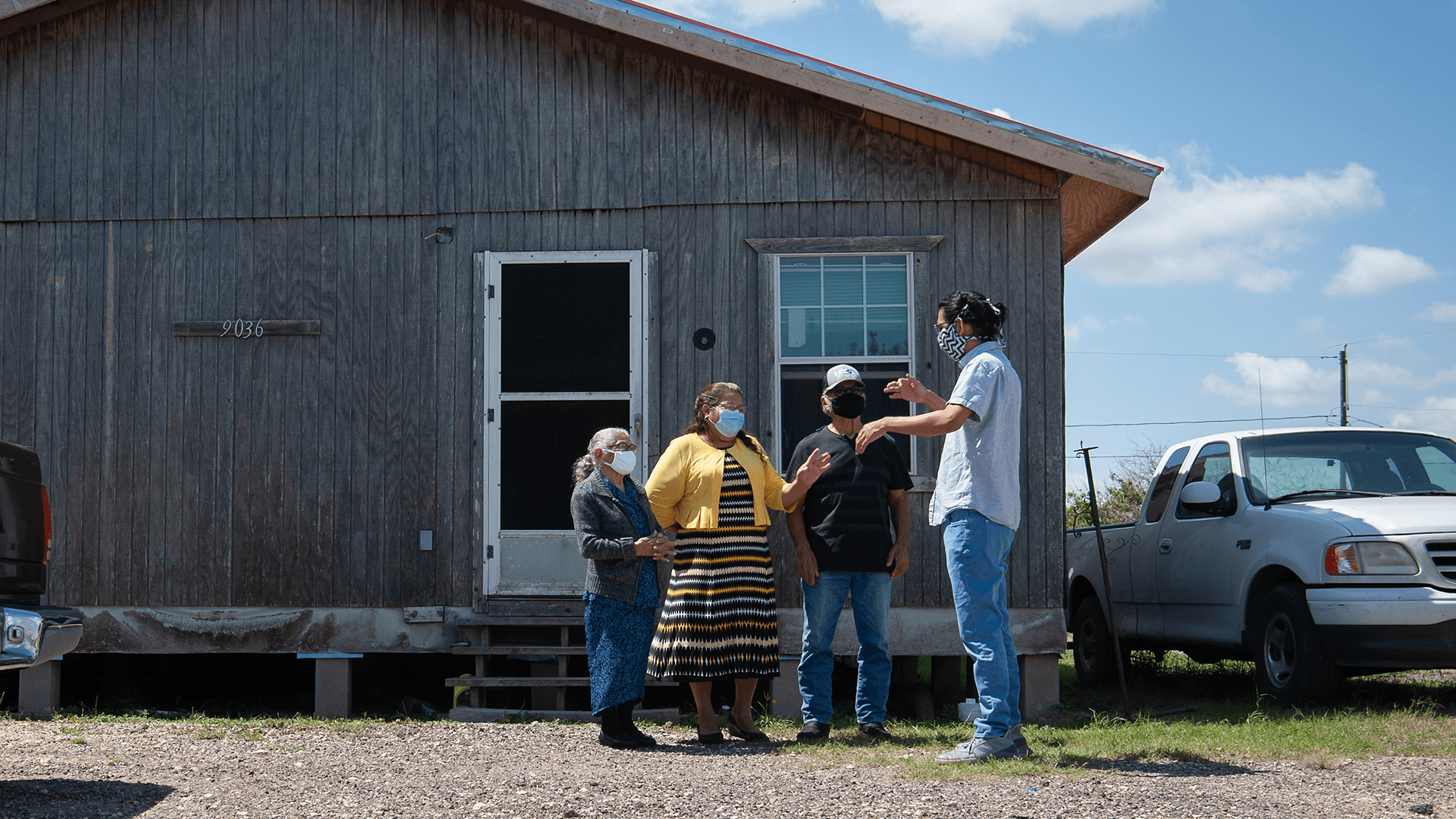

Their ability to continue helping people like Gloria is reflective of CDCB’s deep connections to the community, which have enabled the dedicated staff to turn the challenges of the pandemic into opportunities to introduce a new platform, gain efficiencies, and reach more people. In fact, in recent months, CDCB has doubled the number of people reached, by transitioning current clients to a virtual environment and engaging new clients previously unable to travel to Brownsville for in-person counseling sessions. “Our organization mirrors the communities we serve. We find ways to adapt,” Zoraima Diaz-Pineda, Director of Policy at CDCB.

Although it has been a long process, complicated and protracted by the pandemic, Gloria remains optimistic and looks forward to closing on a home this summer. In thinking about what a suitable home would mean for her aging parents, Erika says, “For us kids, especially my sister and I who are the eldest and the ones who went through the struggle with them since they came to this country, it would honestly mean peace of mind. They’ve worked so hard.”

Gloria Palacios is looking forward to moving into her new home later this year.

The Palacios greet CDCB employee, Josue Ramirez.

Throughout the pandemic, CDCB staff have stayed in close contact with their clients.

Multiple electrical cords hang down across the kitchen to compensate for the lack of working outlets.

Fannie Mae’s Commitment to Affordable Housing

In January 2020, Fannie Mae announced that CDCB was one of the organizations receiving a fee-for-service contract award in its Sustainable Communities Innovation Challenge, a two-year open competition that sought to increase access to affordable housing by spurring innovative ideas to improve the quality of housing, expand access to credit, and increase the supply of affordable housing.

Fannie Mae’s support of CDCB has enabled them to imbed their services with three local employers, integrating their financial and physical health and wealth approach with their financial capability services, and later delivering an app that will enable clients to monitor their progress. Technology-based solutions, including greater social media presence and video communications platforms, have helped CDCB ensure the program expansion was successful and the target client groups were engaged even during the pandemic. Consequently, new clients from this program have grown, including five clients who achieved homebuyer ready status – one of whom recently purchased a home and one who has a house under contract.

The COVID-19 pandemic has brought into plain sight the many disparities that exist in our society, particularly for low-income households and communities of color as they seek safe, stable affordable housing. Through efforts like the Sustainable Communities Initiative and Duty to Serve, Fannie Mae is demonstrating its long-standing commitment to making a difference by executing in the areas we are best suited and by working with partners like CDCB who are equally committed to supporting equitable and affordable housing solutions.

Editor’s note: This is the third of a series of articles from Fannie Mae examining the critical elements of sustainable communities in times of crisis and recovery. Read the first article in the series: Housing & Partnerships, and the second article, Housing & Home.

Business Partners

Homebuyers, Owners, & Renters

- Educational Resources

- Credit Basics

- HomeView Homeownership Education Course

- HomePath - Search for Homes

- Make Your Rent Count