Lack of Mortgage Focus Complicates Home Purchase: An Ethnographic Study Among Low- and Moderate-Income Households

Buying a home and financing that purchase with a mortgage is one of the largest financial decisions that a household will make during its lifetime. In particular, for consumers with fewer financial assets, purchasing a home will result in being far more leveraged than when they rented and compared to other homeowners. In our prior research, low- and moderate-income Americans and renters reported that saving for a down payment and insufficient credit history are the biggest barriers to obtaining a home purchase mortgage.1 Confounding this challenge is the fact that many consumers are not aware of their credit scores or the scores and down payment amounts that lenders require to qualify for a mortgage.2 In other survey work, we have found that consumers tend to leave insufficient time to shop around for their mortgage, focusing on other aspects of the home buying process.3

Buying a home and financing that purchase with a mortgage is one of the largest financial decisions that a household will make during its lifetime. In particular, for consumers with fewer financial assets, purchasing a home will result in being far more leveraged than when they rented and compared to other homeowners. In our prior research, low- and moderate-income Americans and renters reported that saving for a down payment and insufficient credit history are the biggest barriers to obtaining a home purchase mortgage.1 Confounding this challenge is the fact that many consumers are not aware of their credit scores or the scores and down payment amounts that lenders require to qualify for a mortgage.2 In other survey work, we have found that consumers tend to leave insufficient time to shop around for their mortgage, focusing on other aspects of the home buying process.3

To gain additional insights and assist in the interpretation of the results of these various surveys, in this study, we employed an ethnographic approach. This allows us to follow a small group of low- and moderate-income households over a period of months during which they were actively engaged in activities that they hoped would result in a successful transition to homeownership.4 While the tradeoff in this methodology is a small sample size for far greater qualitative information, the results will inform our future survey work.

Key findings include:

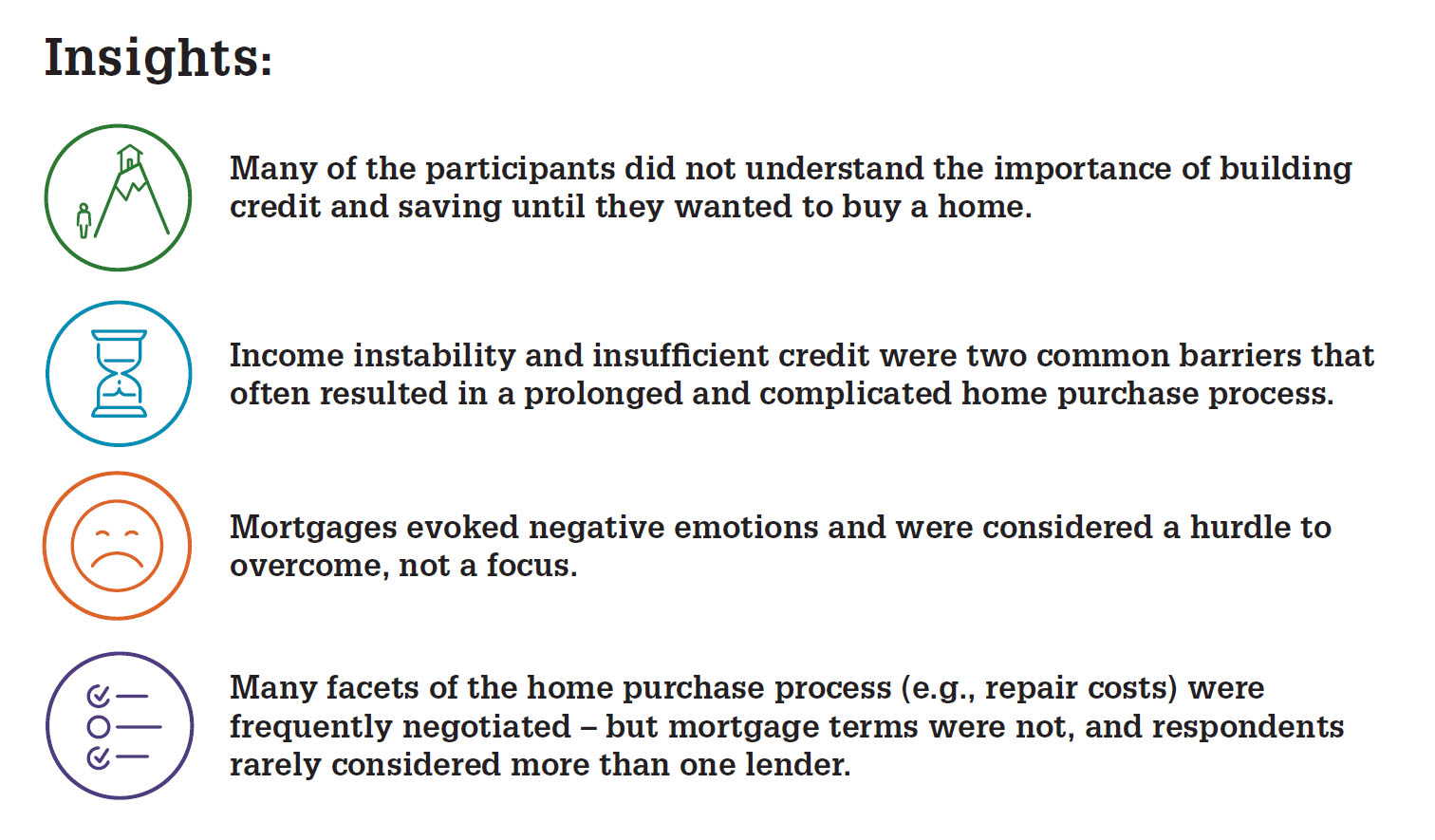

- Research participants faced a number of barriers such as income instability and insufficient credit, resulting in a prolonged and complicated home purchase process. About half of the research participants were able to buy a house at the completion of the research, while the other half had to go back to the preparation phase such as building credit or income history and budgeting.

- Research participants considered the mortgage as a hurdle to overcome throughout a time-pressured home purchase process, not a focus. Emotions around obtaining a mortgage ranged from neutral to negative (e.g., frustrating, overwhelming, and intimidating).

- During the entire home purchase process, research participants focused overwhelmingly on the home search (e.g., location and home features) rather than the mortgage (e.g., how to get a mortgage, what lenders to work with, and when to get started).

- In the early stages (before getting pre-qualified or pre-approved), research participants had vague ideas about mortgages.

- Some mortgage knowledge started to form once they began the pre-approval process. However, once prospective homebuyers selected a lender for a pre-approval, they rarely re-evaluated lenders or mortgage choices.

- Research participants negotiated many facets of the home purchase (e.g., closing time and repair costs), but not the mortgage terms. Their selection of lenders focused on who could get them a mortgage by the deadline, allowing no time for comparison shopping.

In the current study, some research participants did not realize the importance of building credit and saving until they wanted to buy a home. Some had to delay their home purchase and spent another year in building or repairing their credit or adding to their savings before they could start again, making the whole home purchase journey last for more than two years. In addition to a lack of mortgage knowledge – as shown in prior studies – here, too, we see evidence that consumers engage with the mortgage market too late in their home buying journey and often fail to shop around. These results highlight consumer benefits of becoming informed about mortgage options and requirements at the beginning of the home buying process.

To learn more, read our full study findings, "Lack of Mortgage Focus Complicates Home Purchase."

Mark Palim

Deputy Chief Economist and Vice President

Economic and Strategic Research

May 24, 2018

The author thanks Anna Jefferson, Hannah Thomas, and other researchers at Abt Associates in conducting the study. The author also thanks Anne McCulloch, Joe Weisbord, Steve Deggendorf, and Li-Ning Huang for valuable feedback in the design of the study and the creation of this commentary. Of course, all errors and omissions remain the responsibility of the author.

Opinions, analyses, estimates, forecasts and other views of Fannie Mae's Economic & Strategic Research (ESR) Group or of research participants reflected in this commentary should not be construed as indicating Fannie Mae's business prospects or expected results, are based on a number of assumptions, and are subject to change without notice. How this information affects Fannie Mae will depend on many factors. Although the ESR group bases its opinions, analyses, estimates, forecasts and other views on information it considers reliable, it does not guarantee that the information provided in this commentary is accurate, current or suitable for any particular purpose. Changes in the assumptions or the information underlying these views could produce materially different results. The analyses, opinions, estimates, forecasts and other views published by the ESR group represent the views of that group as of the date indicated and do not necessarily represent the views of Fannie Mae or its management.

1Fannie Mae National Housing Survey®, Data Summary, Table q23ba - What would be your biggest obstacle to getting a mortgage to purchase or refinance a home today? https://www.fanniemae.com/resources/file/research/housingsurvey/xls/nhs-022018-datasummary.xlsx

2 "What do consumers know about mortgage qualification criteria?" Fannie Mae, Dec. 2015, https://www.fanniemae.com/resources/file/research/housingsurvey/pdf/consumer-study-121015.pdf

3 "Consumers' Mortgage Shopping Experience," Consumer Finance Protection Bureau, Jan. 2015, https://files.consumerfinance.gov/f/201501_cfpb_consumers-mortgage-shopping-experience.pdf

"What is the Mortgage Shopping Experience of Today’s Homebuyer?" Fannie Mae, April 2015, https://www.fanniemae.com/resources/file/research/housingsurvey/pdf/apr2015-topicanalysis-presentation.pdf

4Abt Associates was commissioned by Fannie Mae to conduct this study. A total of 14 low- and moderate-income prospective first-time homebuyers participated in this research, throughout a 4-9 month period, depending on their stage in home buying, with 10 in greater Boston, MA, and four in greater Knoxville, TN. Ethnography method with multiple data-collection approaches was used, including three onsite (mostly in their own homes) in-depth one-on-one interviews (about 10 hours for each participant), video diaries (up to weekly), pulse surveys, and research participants' mortgage documents. Incoming data were analyzed iteratively, so interview and survey questions could be tailored to get the most complete picture of a participant’s experience. All participants, when joining the study, were not pre-qualified for mortgages, to allow us to track their mortgage-shopping journey from the early stage of home purchase.