Bridging the Gap: The Value of Financial Coaching

Linda Griffin lost her job last year, and then she lost her car. But the 28-year-old single mother had something that many women in her circumstances do not: an emergency savings account. Griffin was able to cover her rent and put food on the table until she was re-hired as a compliance analyst at a Dallas dental chain, a job from which she had been furloughed for four stressful, long months.

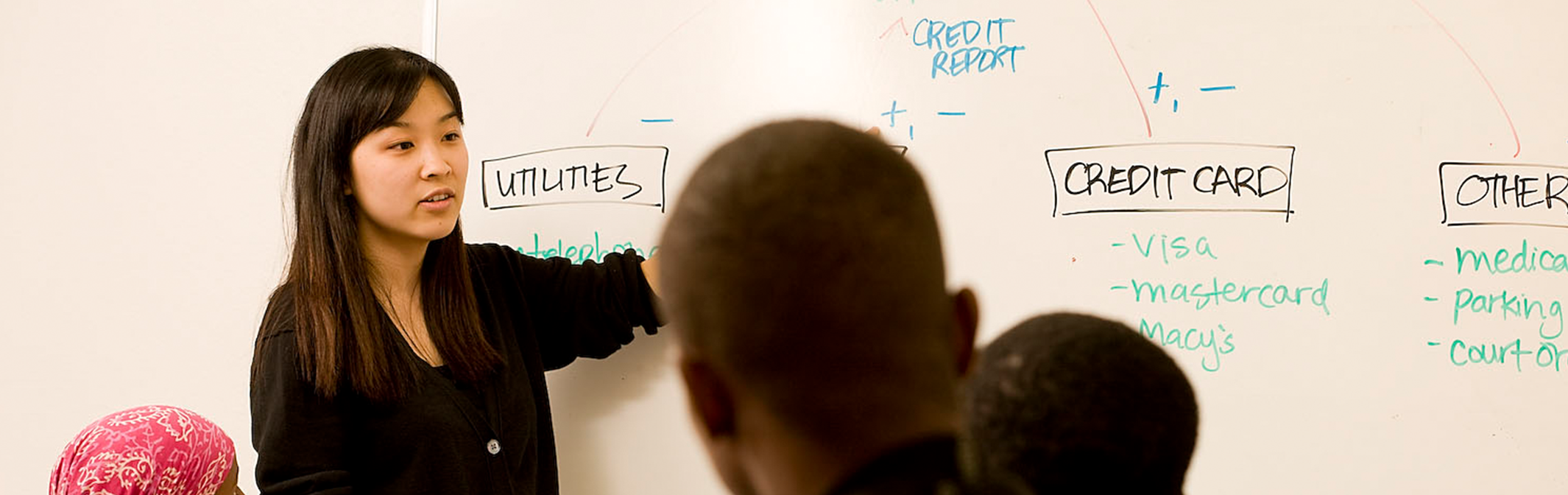

Griffin says she would have never had adequate savings had it not been for a series of financial coaching sessions that the owner of her apartment building in north Dallas provided for free. The partnership between Comunidad Partners and Veritas Impact Partners, a Dallas-based not-for-profit that provides on-site resident services — including telehealth, youth education support, and financial coaching — helps keep cost-burdened, working families afloat.

Veritas’ Director of Resident Engagement Amanda De la Cruz worked with Griffin and other residents ― many of whom have never received financial coaching in their lives ― to give them tips on how to set aside money. “I just help them think about little ways they can start making changes,” De la Cruz explained, “like saving half of your tax refund, or even just starting by cutting out some costs on soda.” De la Cruz added, “Little changes can really help you think differently.”

Resident by resident, and often living room by living room, Veritas’ CEO Jennifer Searles says her team uses “authentic, radical, personal relationships to empower residents, take them out of survival mode, and introduce them to new, inspiring pathways.”

Searles describes the monthly resident council meetings they convene as a series of conversations about “teaching ourselves to take care of our own assets, whether it’s our health or our financial assets.” Sessions have included the importance of renters insurance, budgeting for groceries, and even tips on starting side jobs for extra income.

Amanda is really the first financial coach that I ever had. I’m kind of new to this, and I’m so thankful, because it’s really been a big help.

help

With 38% of people in the U.S. unable to cover a $1,000 emergency,* coaching sessions provide small stepping-stones to financial stability.

*Source: Bankrate survey, December 2020.

Making the case for homeownership

Expanding financial education is also a way to get more people on a pathway to homeownership. At Fannie Mae’s recent “Bridging the Gap” event, which explored the persistent racial inequities in the U.S. housing system and solutions for addressing them, Fannie Mae leadership joined Urban Institute President Sarah Rosen Wartell to examine the widening gap in homeownership rates between white and Black people. Since the Great Recession, that gap has increased to its highest level in 50 years. That’s particularly problematic because homeownership is still a key way to build wealth.

“Wealth amassed in homes helps fuel small business, skills and college education, and more secure retirements,” said Rosen Wartell. “And too often, housing wealth allows access to good schools.”

For Katrina Jones, Fannie Mae’s VP of Housing Equity Strategy and Impact, homeownership is a point of pride in her family, since the land that her grandfather bought in 1920 is still in her family today.

My grandfather could not read, he could not write, so we have the original mortgage with his mark, the X. And I share that story because it's a personal tribute to why homeownership for people of color and their families is so critical. It is the primary mechanism for us to go and build wealth that we pass on generation to generation.

With limited housing inventory and robust buyer demand, homeownership may feel more out of reach than ever, but financial coaching can “teach people the value of credit, teach them the value of a savings account, teach them how to become banked,” explained Jones.

Former CEO Hugh Frater said, “We should begin educating folks about financial planning, budgeting, teaching them the basics about renting, about homeownership, about the entire journey.”

To help people on that journey, Fannie Mae is working with Local Initiatives Support Corporation (LISC), a large community development financial institution that makes grants, loans, and equity investments in communities across the country to catalyze opportunity.

Our job is to help people fundamentally change their economic condition and build a pathway out of poverty.

help

Denise Scott, LISC’s EVP of Programs, is well aware that homeownership is out of reach for many people in the U.S., but she says financial coaching, offered through LISC’s network of more than 110 Financial Opportunity Centers® (FOCs) in more than 30 cities across the country, helps meet individuals where they are and helps them “think beyond the immediate circumstance that they’re in, to imagine a future with brighter opportunities, and to reach that future.”

In 2020, FOC coaches helped more than 13,000 individuals achieve key financial outcomes, including securing employment, increasing their monthly cash flow, raising their FICO scores, and improving their net worth: impressive results for an economically tumultuous year. “We’ve seen the needle moving for families who are getting the coaching,” Scott explained. “It doesn't happen overnight, but we see movement.” Fannie Mae and LISC are working to identify underserved communities across the country where financial coaching is most likely to lead to homeownership.

Scott said some of LISC’s clients who may be on the path to homeownership remain concerned about predatory lenders, incorrect appraisals, and whether they’re being offered the best rates. Fannie Mae’s research indicates a disconnect between what prospective homeowners think they need in order to buy a home, and what the typical mortgage requirements actually are. The education and supports offered by FOC coaches help clients avoid these pitfalls and clears up misperceptions.

Did You Know?

The majority of consumers don’t know the credit score, down payment, or debt-to-income ratio requirements from mortgage lenders.

- Credit scores of 580 are acceptable for certain loans.

- Down payments can be as little as 3%.

- Debt-to-income ratios can be 50%.

Source: Consumer Mortgage Understanding Infographic — June 2019 (fanniemae.com).

Fannie Mae EVP and Chief Administrative Officer Jeff Hayward said, “We are creating three- to five-year commitments with some of our racial equity lender partners, including U.S. Bank and Prosperity Mortgage, to help combat systemic racism in housing.” Hayward added, “Together, we will focus on youth and adult financial education and homebuyer information; increasing minority representation in the industry; reducing the Black homeownership gap; and changing the trajectory of Black wealth by expanding sustainable homeownership.”

One of Fannie Mae’s key partners, U.S. Bank, is working to help Black consumers build equity and wealth through its multi-pillared initiative to advance Black homeownership. The program, which will launch in September nationwide, will include enhanced adult financial education through local community partners. Lenny McNeill, EVP of National Strategic Markets for U.S. Bank, says, “We appreciate the opportunity to partner with Fannie Mae in a joint effort focused on creating and providing racial equity in housing. McNeill added, “Let’s go to work!”

Your Own Story

To educate potential homebuyers about the homebuying process, Fannie Mae has produced the Your Own Story campaign, featuring a series of videos, a financial calculator to help individuals determine what they can afford, and printable homebuyer checklists.

“What I love about Your Own Story is it’s not only unpacking what you need to do, but it’s also the order which you need to do it in,” said Jones. “It lets you drive at your own pace.” Individuals can also access HUD-approved housing counselors and research down payment assistance options.

“And the other thing I love about Your Own Story,” added Jones, “and this is one of the things I preach to my family members all the time: Don't go looking for a house until you know what you're qualified for!”

Back in Dallas, Linda Griffin has been doing her own research on the mortgage process and is happy to realize she doesn’t need to save as much for a down payment as she originally thought. She said she is lucky to live in an area where condominiums in her price range are available.

“I love my apartment, I love the community I’m in,” Griffin said. “But eventually, I would like to have our own home, so it’s been really helpful to have the building blocks to get to that ultimate goal.”

Business Partners

Homebuyers, Owners, & Renters

- Educational Resources

- Credit Basics

- HomeView Homeownership Education Course

- HomePath - Search for Homes

- Make Your Rent Count