Technological Investment Necessary in Evolving Mortgage Landscape, Lenders Say

Mortgage lenders continue to cite “consumer-facing technology” as the most important business priority to maintain competitiveness, according to Fannie Mae’s Mortgage Lender Sentiment Survey® (MLSS). Additionally, most lenders consider “online business-to-consumer lenders” as their biggest competitor, citing their advantages in technology.

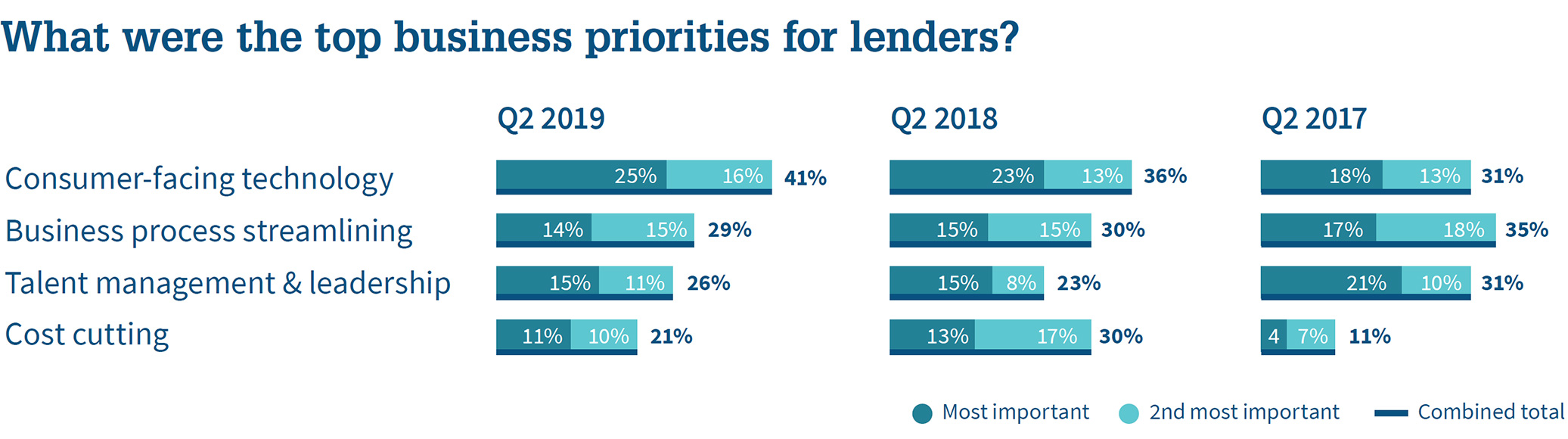

Mortgage lenders continue to cite “consumer-facing technology” as the most important business priority to maintain competitiveness, according to Fannie Mae’s Mortgage Lender Sentiment Survey® (MLSS). Additionally, most lenders consider “online business-to-consumer lenders” as their biggest competitor, citing their advantages in technology.

The mortgage industry has faced a number of challenges in recent years. Technological advancements, demographic changes, increased competition, and lack of entry-level housing stock have applied pressure to growth and profitability. Over the past two years, lenders have continuously pointed to “competition from other lenders” as the most significant drag on their profit margin outlook.1 Through its MLSS, Fannie Mae’s Economic & Strategic Research Group surveyed over 200 senior mortgage executives to better understand their evolving business priorities and strategies in this more competitive marketplace.

For three consecutive years, lenders have cited “consumer-facing technology” and “business process streamlining” as their top two business priorities. Moreover, the importance of “consumer-facing technology” has grown steadily from 2017 to 2019. Meanwhile, the importance of “cost-cutting,” another commonly cited business priority, fell this year after jumping in 2018, when rising interest rates and dropping volume forced many lenders to pare back to maintain profitability. Lenders have most frequently pointed to personnel expenses, such as back-office staff and administrative expenses, as the likeliest areas in which to save money. By contrast, very few lenders say they would cut back on technology-related investments, including corporate IT, consumer-facing technology, and back-end processing. For those lenders who have cited reducing staff as a cost-cutting priority, it likely reflects the impact of enhanced productivity due to investments in technology.

Lenders’ business priorities also appear to be in line with their assessment of market threats. A majority expect “online business-to-consumer lenders” to be their biggest competitor over the next five years, followed by traditional financial institutions with branches, online real estate service providers, and mortgage brokers. Many pointed to B-to-C lenders’ advantages in technology, scalability, and advertising and technology budgets.

In order to be better equipped to deal with market fluctuations, lenders appear to be trending toward making investments to improve their customer experience while reducing the cost to manufacture mortgage loans on the back end. However, new entrants are challenging existing market dynamics; among these are digital banking startups focused on building a simpler digital experience for consumers and a more streamlined back-end system for employees. Traditional lenders report that online lenders present the largest threat to their business going forward.

As a result, lenders believe that their biggest opportunity lies in re-engineering their processes to be competitive in similar ways. The extent to which this type of simple digital banking model can be operationalized within a complex mortgage ecosystem remains to be seen, but investments to that end continue to be made.

To learn more, read the full research deck, “How Are Lenders’ Business Priorities Evolving to Compete Against Industry Competition,” or check out our easy-to-read infographic.

Andrew Peters

VP, Single-Family Strategy & Insights

July 18, 2019

The author thanks Steve Deggendorf and Li-Ning Huang for valuable contributions in the creation of this commentary and the design of the research. Of course, all errors and omissions remain the responsibility of the author.

Opinions, analyses, estimates, forecasts and other views reflected in this commentary should not be construed as indicating Fannie Mae's business prospects or expected results, are based on a number of assumptions, and are subject to change without notice. How this information affects Fannie Mae will depend on many factors. Changes in the assumptions or the information underlying these views could produce materially different results.

1 Mortgage Lender Sentiment Survey, https://www.fanniemae.com/portal/research-insights/surveys/mortgage-lender-sentiment-survey.html

Full Page Infographic

MLSS Special Topic Report