Lenders describe COVID-19-related challenges and business priorities

The COVID-19 outbreak and associated public health response has had a particularly negative impact on consumer-facing businesses. Despite this unprecedented headwind, lenders and servicers adapted rapidly to meet a surge in refinance applications, implement nationwide forbearance programs put in place by Fannie Mae and Freddie Mac and subsequently mandated under the CARES Act1, and adopt policy updates for loan eligibility and servicing requirements2. In early May, Fannie Mae surveyed more than 200 senior mortgage executives to identify the challenges they faced in meeting the needs of their borrowers during this difficult time.

More specifically, the survey asked lenders two primary questions: 1) What are the biggest challenges that they've faced in loan origination and mortgage servicing in response to COVID-19?; and 2) What are their most important business priorities, and to what extent has COVID-19 influenced those priorities?

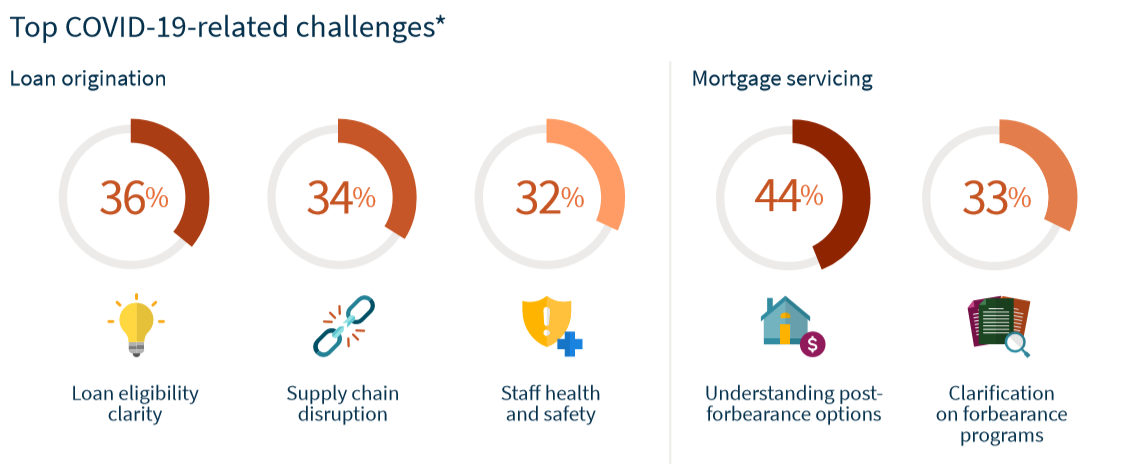

As the industry contended with a litany of policy updates, temporary servicing and origination flexibilities, new state and local guidance, and federal CARES Act requirements, the leading challenges identified by lenders were: 1) gaining clarity from secondary-market investors around updates to loan eligibility guidelines; 2) navigating supply chain disruptions; and 3) ensuring the health and safety of staff.

Initial disruptions to the loan origination process included delays in obtaining employment verification, appraisals, title searches, and scheduling closings. These delays frequently resulted from a combination of the closure of other businesses, reduced staff levels or hours, and the fear of virus contagion. Lenders also noted the high number of policy changes, and that the changes were often difficult to implement.

For mortgage servicers3, the leading challenge cited was "understanding and navigating post-forbearance options for distressed borrowers," followed by "gaining clarifications on forbearance programs." Servicers noted that the forbearance programs were developed quickly and in parallel across investors, making it more difficult to manage workflows. Furthermore, some servicers commented that, because forbearance policies were being continuously updated, they had difficulty providing inquiring borrowers with the most current information.

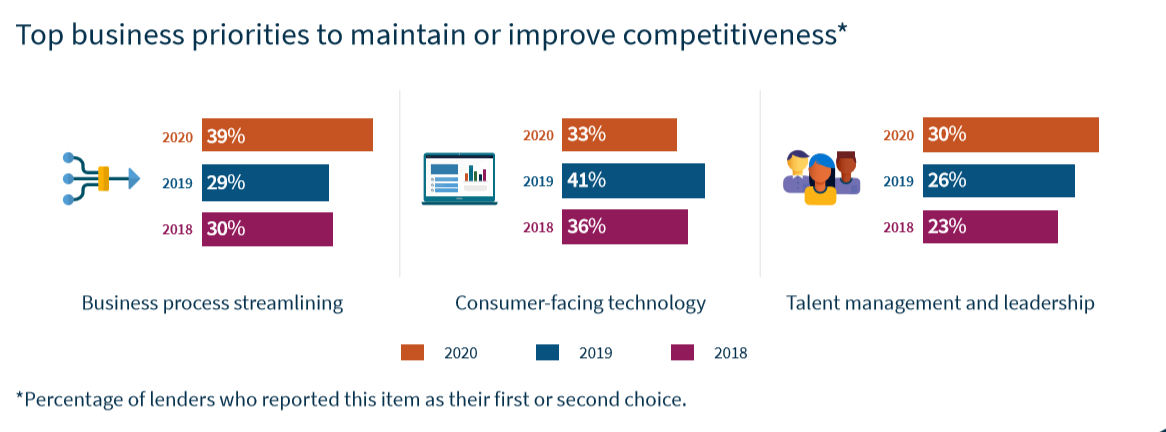

For the fourth year in a row, mortgage lenders cited "business process streamlining" and "consumer-facing technology" as the two most important business priorities for the year. In 2020, the importance of "business process streamlining" rose significantly – from 29% to 39% -- and is now clearly lenders’ most important priority.

In response to COVID-19, some lenders noted the increased threat of potential repurchases and margin calls. Additionally, lenders cited handling evolving regulatory and investor requirements, managing cash advances, and preparing for loss mitigation programs as top challenges. As a result, lenders noted the need for loan origination and compliance efficiency.

Lenders' investments in technology over the past few years played an important part in their ability to handle increased origination and servicing workloads. This year, technology was notably absent from lenders’ list of leading challenges but remains a focus of their 2020 business priorities, along with process streamlining. Presumably, the prioritization of process streamlining by lenders is due in part to the recognition that at some point the current refinance boom will come to an end, and lenders will need to be more efficient in order to remain profitable in a potentially thinner origination market.

To learn more, read our Fannie Mae Mortgage Lender Sentiment Survey Special Topic Report, "COVID-19 Challenges and Its Impact on Lenders' Business Priorities."

Mark Palim

VP and Deputy Chief Economist

June 29, 2020

The author thanks Ahmet Hacikura at Oliver Wyman, Michael Cafferky, Bill Cleary, Cyndi Danko, Steve Deggendorf, Doug Duncan, Li-Ning Huang, Dan Miller, Caroline Patane, Colette Porter, and Dana Schlafman for valuable contributions in the design of the research creation and creation of this commentary. Of course, all errors and omissions remain the responsibility of the author.

Opinions, analyses, estimates, forecasts and other views of Fannie Mae's Economic & Strategic Research (ESR) group or survey respondents reflected in this commentary should not be construed as indicating Fannie Mae's business prospects or expected results, are based on a number of assumptions, and are subject to change without notice. How this information affects Fannie Mae will depend on many factors. Changes in the assumptions or the information underlying these views could produce materially different results. The analyses, opinions, estimates, forecasts, and other views published by the ESR group represent the views of that group or survey respondents as of the date indicated and do not necessarily represent the views of Fannie Mae or its management.

1 The federal government enacted the Coronavirus Aid, Relief, and Economic Security (CARES) Act on Mar. 27, 2020. The CARES Act includes provisions that provide assistance to some affected mortgage borrowers and renters. For details, please see https://www.consumerfinance.gov/coronavirus/cares-act-mortgage-forbearance-what-you-need-know/ https://www.fhfa.gov/Homeownersbuyer/MortgageAssistance/Pages/Coronavirus-Assistance-Information.aspx.

2 Fannie Mae and Freddie Mac (together, the "GSEs"), the Federal Housing Administration ("FHA") and the Department of Veterans Affairs ("VA") have issued various updates regarding changes to their origination guidelines during the COVID-19 outbreak. Details are available on their websites.

3 Servicers in the study refer to lenders who self-reported that they retain Mortgage Servicing Rights (MSRs). Servicing-related survey questions are asked only among lenders with MSRs retained.

Full Page Infographic

MLSS Special Topic Report