Commentary - Deggendorf, October 30th 2015

Mobile devices are widely and increasingly used for a variety of transactions, including mobile payments and banking. Mobile activity is less common in the mortgage space than other consumer finance market segments, but the opportunity is promising. However, the lower priority that lenders are placing on mobile channels, and the differences in lender and consumer views on mobile tool functionality, could place lenders at risk of not meeting consumer demand or encouraging new entrants to address this growing demand at the expense of existing firms. Getting the right mix of traditional (person-to-person), online, and mobile channels and tools may be a key to future success.

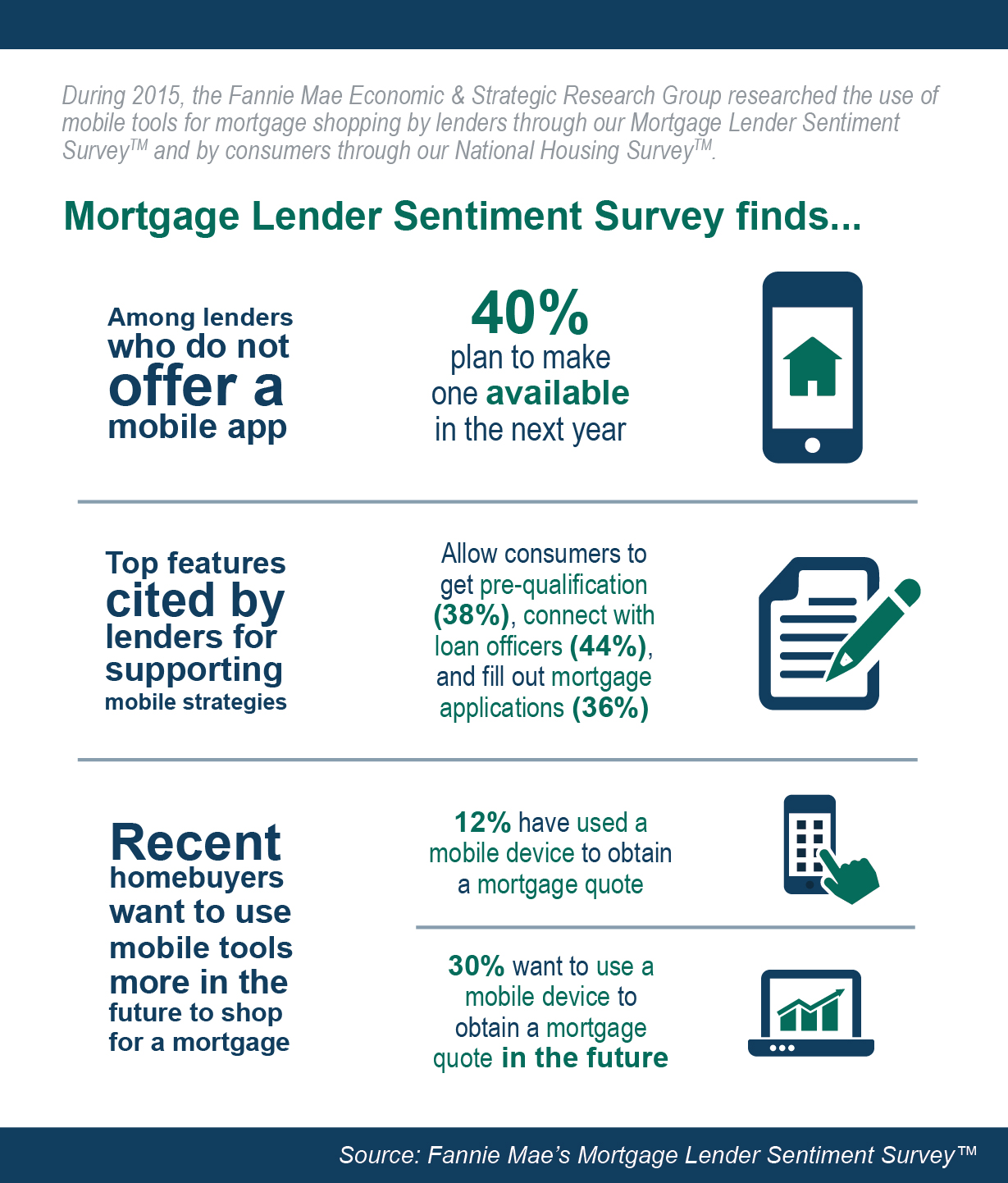

During 2015, we researched the use of mobile tools for mortgage shopping by consumers through our National Housing Survey™ (NHS) study, Consumer Attitudes about Getting a Mortgage Online and via Mobile Technology, and by lenders through our Mortgage Lender Sentiment Survey™ (MLSS), Lenders’ Consumer-Facing Mobile Technology Priorities: Are Mortgage Lenders Missing Out on Mobile Opportunities? We found that homebuyers in increasing numbers are going online to get their mortgage using both personal computer and newer mobile-based technologies. In particular, our NHS data suggest that consumers’ desire to shop and apply for a mortgage via a mobile device (smartphones and tablets) in the future is more than twice the current usage.

In MLSS responses, lenders reported that they still favor more traditional channels (loan officers, branches, and third-party partnerships) to digital channels (Figure 1), and most do not yet offer a mobile app that enables consumers to shop for a home or obtain a mortgage. Most lenders employ a combination of traditional and digital marketing channels to advertise their mortgage products, but mobile apps are used much less often. Lenders also say they will continue to emphasize investment in traditional over digital, and especially mobile, channels in the future.

Figure 1. Lender Current Top Marketing Channels and Future Channel Investment Priorities

Approximately three out of four lenders do not offer a mobile app to help consumers shop for a mortgage. Forty percent of those lenders who do not offer a mobile app plan to make one available over the next 12 months. The one-third of lenders not developing an app cite the high cost of IT investment, information security risks, compliance issues, and slow consumer adoption as their top reasons. Another quarter of lenders who do not offer a mobile app do not know or are unsure about their next steps to build a mobile app.

Results from the NHS show that recent homebuyers’ appetite for using mobile devices for mortgage shopping may imply faster adoption than what many lenders assume, especially those who are not building a mobile mortgage app (Figure 2). Although only 12 percent and 6 percent of recent homebuyers, respectively, say they have used mobile devices to get a mortgage quote and to fill out a mortgage application, 30 percent and 20 percent, respectively, say they would like to use a mobile device in the future to perform these mortgage activities.

Figure 2. Lenders and Consumers Differ in Mobile Adoption Expectations

In addition, consumers’ and lenders’ mobile functionality preferences show some gaps (Figure 3). Whether lenders currently have a mobile app or not, they say the most important mobile functionality include allowing consumers to get pre-qualification, connect with loan officers, fill out application forms, and track the application process. On the other hand, consumers are more interested in using mobile devices to obtain a mortgage quote, giving this functionality a much greater priority than lenders do. Consumers also are less interested in using mobile devices to fill out a mortgage application than lenders seem to be in providing this functionality.

Figure 3. Lender and Consumer Mobile Functionality Preferences

Security concerns are a common theme among both consumers and lenders. Almost one-third of lenders cite security risks as the primary reason for not developing an app, and online security among recent homebuyers is the biggest concern (over 50 percent) related to applying for and closing a mortgage online.

Our research shows that there remains an important role for face-to-face contact. Many consumers still prefer speaking to an expert at certain points during the mortgage shopping process. At the same time, mortgage lenders should consider the appropriate mix of traditional, online, and mobile mortgage channels and functionality to address the evolving consumer preferences of the particular market segments they serve. The NHS consumer study, Consumer Attitudes about Getting a Mortgage Online and via Mobile Technology, shows that those with a college education, higher income, and younger age drive the use of online and mobile tools in mortgage shopping among recent borrowers. This information may be helpful to those considering enhancing their mix of channels and functionality for their market segments.

Steve Deggendorf

Director, Business Strategy

Economic & Strategic Research Group

October 30, 2015

The author thanks Qiang Cai, Li-Ning Huang, and Sarah Shahdad for their valuable research and comments in the creation of this commentary. Of course, all errors and omissions remain the responsibility of the author.

Opinions, analyses, estimates, forecasts and other views of Fannie Mae's Economic and Strategic Research (ESR) Group included in these materials should not be construed as indicating Fannie Mae's business prospects or expected results, are based on a number of assumptions, and are subject to change without notice. How this information affects Fannie Mae will depend on many factors. Although the ESR group bases its opinions, analyses, estimates, forecasts and other views on information it considers reliable, it does not guarantee that the information provided in these materials is accurate, current or suitable for any particular purpose. Changes in the assumptions or the information underlying these views could produce materially different results. The analyses, opinions, estimates, forecasts and other views published by the ESR group represent the views of that group as of the date indicated and do not necessarily represent the views of Fannie Mae or its management.

Business Partners

Homebuyers, Owners, & Renters

- Educational Resources

- Credit Basics

- HomeView Homeownership Education Course

- HomePath - Search for Homes

- Make Your Rent Count