APIs Are Reshaping Business Strategy

Businesses are increasingly leveraging digital technologies to reduce errors and costs, speed up transactions, and drive richer and better customer service. Examples of digital technologies attracting interest include Application Programming Interfaces (APIs)1, Artificial Intelligence (AI), and distributed ledger technology (also known as "blockchain")2. Over the past few years, more and more companies, including Google Maps, PayPal, OpenTable, and Netflix, have leveraged APIs to help deliver a seamless customer experience via easier collaboration.3 Additionally, MasterCard is experimenting with AI bots to allow consumers to transact, manage finances, and shop via messaging platforms.

Businesses are increasingly leveraging digital technologies to reduce errors and costs, speed up transactions, and drive richer and better customer service. Examples of digital technologies attracting interest include Application Programming Interfaces (APIs)1, Artificial Intelligence (AI), and distributed ledger technology (also known as "blockchain")2. Over the past few years, more and more companies, including Google Maps, PayPal, OpenTable, and Netflix, have leveraged APIs to help deliver a seamless customer experience via easier collaboration.3 Additionally, MasterCard is experimenting with AI bots to allow consumers to transact, manage finances, and shop via messaging platforms.

Fannie Mae's Economic & Strategic Research Group (ESR) surveyed senior mortgage executives in February through its quarterly Mortgage Lender Sentiment Survey® to gather the views of lenders about data strategy and technological innovation in general, and, specifically, to understand their experience with two digital technologies: APIs and Chatbots4.

The study revealed the following key findings:

- About three out of five lenders agree that their firm is making the best use of data for their mortgage business. However, only about one-third of lenders say their firm has a formal data strategy, including a dedicated internal data team. Nearly four in 10 lenders say they address data-related activities on an ad-hoc basis.

- The majority of lenders surveyed say they are technology followers, not early adopters. Additionally, about four in 10 think that the pace of technological innovation in the mortgage industry is too slow.

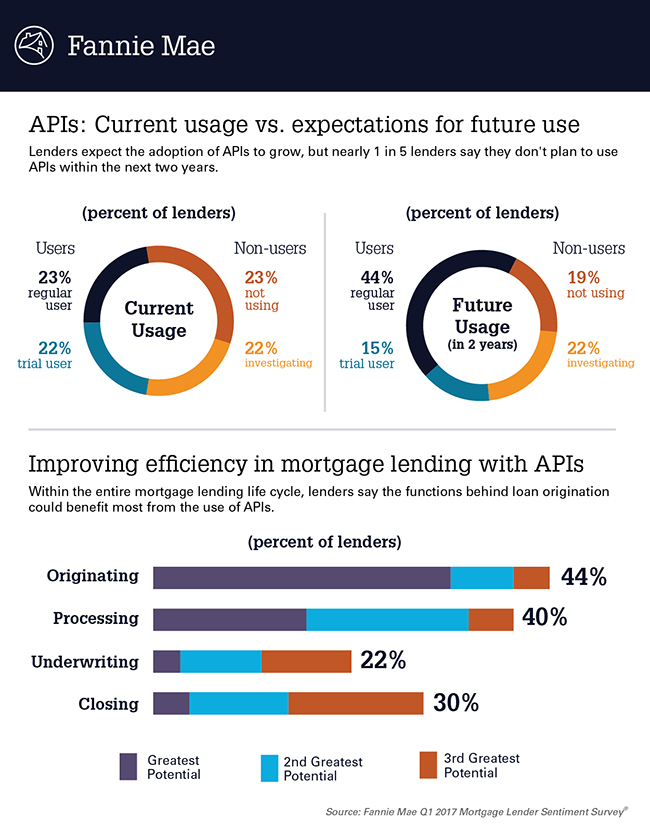

- About half of lenders surveyed have either incorporated APIs into their mortgage process or used them on a trial basis. In contrast, very few lenders say their firm has looked into using Chatbots.

- Lenders expect the adoption of APIs to grow in the future state. However, nearly 20 percent of lenders say they do not plan to use APIs within the next two years.

- Lenders who currently use APIs do so primarily to integrate information, such as appraisals and verifications, with their Loan Origination System and other services within their firm.

- Lenders see loan production (origination, processing, underwriting, and closing) as the greatest area of potential for APIs and Chatbots. Lenders also see the potential for using APIs in paying taxes and insurance from escrow accounts.

Today's consumers demand a simple and streamlined experience in all aspects of their life. However, mortgage transactions are complex, involve many interdependencies, and require extensive collaboration. In other industries, APIs have become a crucial element of business strategies to deliver a seamless customer experience because they make data-sharing easier.

As an example, let's consider the customer experience in planning a night out at a restaurant. Using a mobile phone, the consumer can search for a restaurant on a review site and make a reservation. The consumer then might click on the map to see where the restaurant is located and decide they'd like to order a car service to get there. Conveniently, there is a button to do just that.

That whole series of steps takes just a few minutes. Because the various providers make their functionality available to each other via APIs, the consumer has an integrated and efficient experience, and each of those businesses is able to benefit from the "connection."

APIs are the key to transforming the mortgage experience so it is as simple as the restaurant example. They allow lenders and technology service providers to meet demands in a fast, agile, and scalable way. APIs will reshape how work is done and how companies compete. Lenders who do not expect to adopt APIs in the near future may well find themselves being pushed to the sidelines.

To learn more, read our Fannie Mae Mortgage Lender Sentiment Survey Special Topic Report, "Lenders' Experiences with APIs and Chatbots."

Tracy Stephan

Director, Innovation

May 18, 2017

The author thanks Prabhakar Bhogaraju, Michael Perednis, Ryan Jackson, Burke Spaulding, Tom Seidenstein, Doug Duncan, Steven Deggendorf, and Li-Ning Huang for valuable contributions in the creation of this commentary and the design of the research. Of course, all errors and omissions remain the responsibility of the author.

Opinions, analyses, estimates, forecasts and other views reflected in this commentary should not be construed as indicating Fannie Mae's business prospects or expected results, are based on a number of assumptions, and are subject to change without notice. How this information affects Fannie Mae will depend on many factors. Changes in the assumptions or the information underlying these views could produce materially different results.

1 Application Programming Interfaces (APIs) are software that enables diverse software programs to communicate and work together. Examples include embedding business partners’ APIs such as Zillow, Google Maps, and FedEx location/tracking into a firm’s applications.

2 Distributed ledger technology is a synchronized ledger or database shared across a network. It allows parties to send, receive, and record value of information, without going through third parties.

3 Companies listed here are provided as examples to help illustrate user cases of digital technologies. Fannie Mae does not endorse these companies.

4 Chatbots are software programs, powered by artificial intelligence, that understand and respond to questions and commands. Banks, airlines, and some other industries are developing "virtual assistants" to interact like humans to answer customer questions or help customers complete tasks. For example, Bank of America and MasterCard have announced chatbot tools that allow customers to ask questions about their financial accounts, initiate transactions, and get financial advice via text messages or services like Facebook Messenger and Amazon's Echo tower.