Economic Developments - January 2024

For a PDF version of this report, click here.

We expect that housing and mortgage markets will begin trending toward a more typical pattern in 2024 after experiencing turbulent oscillations and divergence from historical relationships over the past few years. The volatility of mortgage rates, combined with reverberating effects stemming from the pandemic, led to an odd combination in 2023 of the lowest pace of existing home sales since the Great Financial Crisis and depressed mortgage originations, but paired with solid home price growth and robust new home construction. We expect many of the dynamics prevalent in 2023, such as stretched affordability, the “lock in effect,” and limited supply, will continue into 2024. However, we believe that moderating mortgage rates, a decelerating economy, and waning effects of the 2020-21 period’s pull-forward of home purchase activity will precipitate an unfreezing of the existing homes market, and therefore a movement toward a more balanced housing market. We believe the start of a recovery in existing home sales will likely occur, along with moderating home price growth and a more stable level of new home construction. Ultimately, we expect growth in mortgage originations, including some improvement in the refinance segment. We forecast 2024 total single-family mortgage originations to be $1.98 trillion in 2024 and $2.44 trillion in 2025, up from $1.50 trillion in 2023. Primarily due to recent easing in financial conditions, we have removed our previous expectation of a 2024 recession from our baseline forecast, though the macroeconomic backdrop is still one of below-trend growth and with a heightened level of uncertainty.

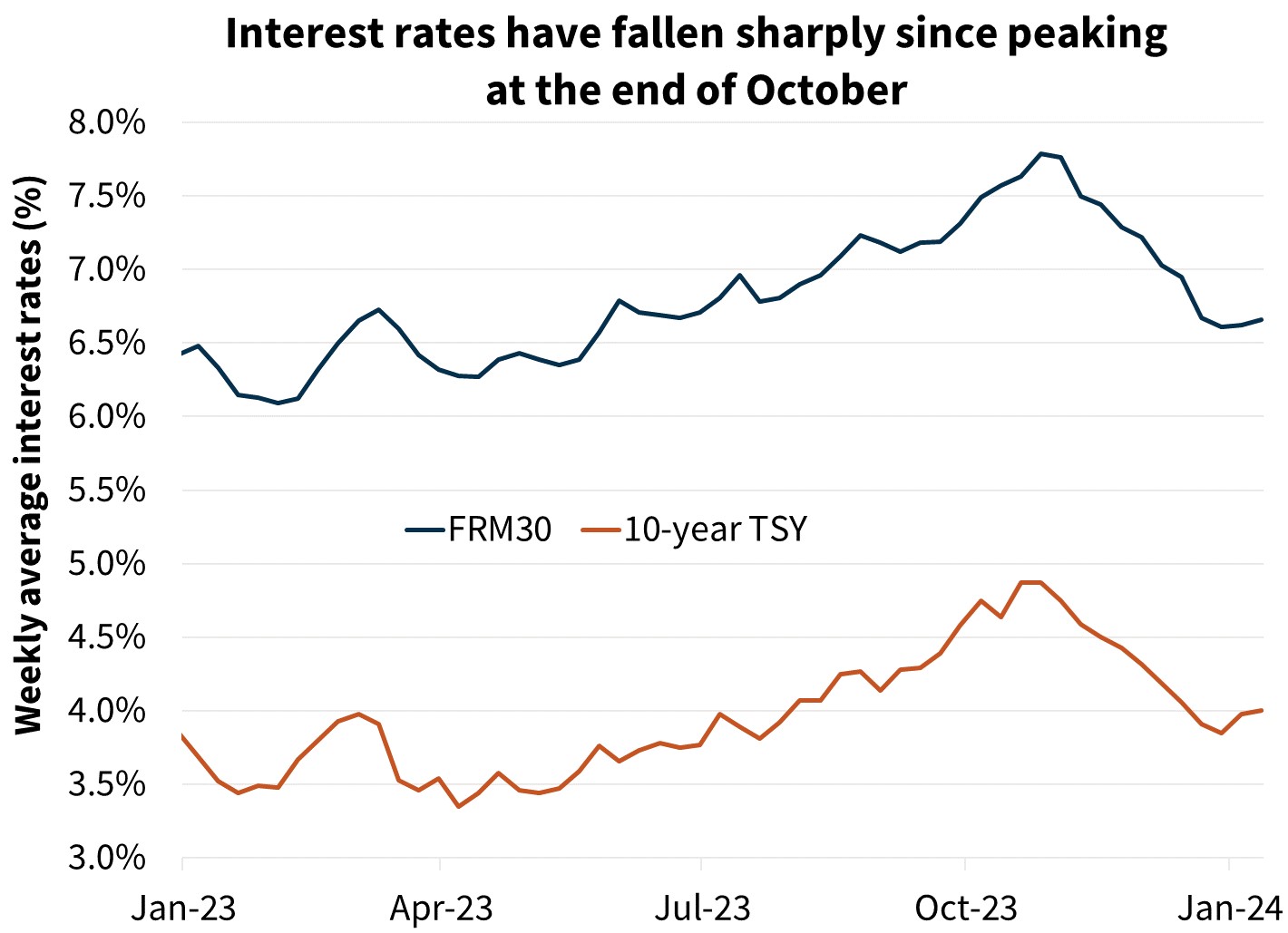

Mortgage Rates Expected to Moderate Toward a More Normal Level

Existing Home Sales Market Will Begin to Unfreeze

While we expect affordability will remain stretched and the supply of homes for sale tight, an easing in mortgage rates is expected to begin thawing the existing home sales market, which was held back in 2023 by strong lock-in effects. Furthermore, many homebuyers and sellers in 2020 and 2021 likely pulled forward their moving intentions to take advantage of low mortgage rates and remote working options following the COVID-19 pandemic, reducing the pool of homeowners wishing to move soon thereafter. As time progresses, however, we believe this effect will wane, and when combined with existing homeowners who delayed their moves in 2023 due to high mortgage rates, we expect that a growing number of home sales will occur. While we are still anticipating a comparatively sluggish pace of existing home sales, as affordability and a lack of supply remain challenges to the market, we are forecasting successive quarterly sales increases in 2024 with sales ending the year around 4.5 million annualized units in Q4 compared to the year low of around 3.8 million annualized units in Q4 2023. For the year, we forecast existing sales to rise 3.1 percent in 2024.

Single-Family Home Construction to Remain Strong, but Multifamily Continues its Breather

The strength of single-family home construction surprised to the upside over much of 2023. While the loosening of the existing sales market should help balance homebuyer interest in new and existing homes, the overall housing stock remains limited relative to what historical demographic trends would suggest is required following a decade of underbuilding following the financial crisis. Millennials also still have a few more years of being at the peak first-time homebuying age. Recent data on residential housing construction employment also points to an expanding homebuilding industry. As such, we expect new construction to remain strong, and we project 2024 single-family housing starts to be 5.7 percent higher than in 2023.

In contrast, the slowdown in multifamily construction that began in 2023 will likely continue into 2024. Rent growth has been weak as an historically high flow of new supply enters the market. While we expect solid multifamily construction over the next five years given the ongoing overall lack of housing supply, 2024 is likely to continue to be a breather following a torrid pace of starts in 2022. For the year, we forecast multifamily housing starts to fall 18.3 percent in 2024

Home Price Growth to Moderate

As measured by the Fannie Mae Home Price Index, home prices ended 2023 up 7.1 percent on a Q4/Q4 basis, a strong pace of growth, especially given the surge in mortgage rates over the year and worsening affordability conditions. While moderating mortgage rates going forward will help support home prices, affordability is still going to remain historically challenging. Combined with a cooling labor market, we see the ability of homebuyers to keep pushing prices upward as more limited. The aforementioned unfreezing of the existing home sales market, combined with increasing supply of new homes coming online, should help loosen the market somewhat. We believe slowing or even declining multifamily rents in much of the country will also make the rent vs. buy calculus shift comparatively more favorable to renting multifamily units, reducing upward pressure on single-family home prices.

Mortgage Originations Will Grow Meaningfully, Including Some Signs of Life in Refinance Loans

With an expectation of rising home sales, moderating mortgage rates, a downward drift in the cash share of home sales, and continued positive home price growth, we forecast single-family mortgage origination dollar volume to grow significantly in 2024, albeit from a depressed starting level. We expect 2024 single-family purchase origination volumes will be $1.5 trillion, a 19 percent increase from $1.3 trillion in 2023.

The Economic Backdrop is Looking More Positive, Though Still with Elevated Recession Risk

We have removed our explicit call for a recession in 2024 and replaced it with an expectation of below-trend growth. We have upgraded our 2024 economic outlook from a 0.3 percent Q4/Q4 contraction of real gross domestic product (GDP) to a modest expansion of 1.1 percent.

In our December commentary, we argued that the restrictive stance of monetary policy would need to ease if a downturn were to be prevented. This has occurred following the previously discussed Fed “pivot” in December. The Chicago Fed National Financial Conditions Index currently shows the loosest financial conditions in nearly 11 months, while the loosening of the Goldman Sachs Financial Conditions Index over November and December was the greatest two months of easing in the 40-year-plus history of the index. While monetary policy remains in a restrictive stance in an absolute sense and will still weigh on economic activity, when compared to October, broader financial conditions have eased considerably. Combined with continued solid real income gains in recent months, we have decided to upgrade our growth outlook.

Additionally, the easing of monetary policy opens the door for inflation to possibly reanimate. Despite signs of softening in the labor market, the unemployment rate remains low and average hourly earnings over the past two months have come in hot, highlighting the possibility that a tight labor market could still contribute to inflationary pressures in the future. Further, the recent rise in shipping rates due to attacks on container vessels in the Red Sea risks a reinflation in goods prices. Our baseline forecast continues to show inflation trending toward the Fed’s 2-percent target over the course of the year, but risks to the outlook remain.

Economic Forecast Changes

Economic Growth

Primarily due to easing financial conditions and incoming real income data, we have changed our 2024 recession call to a forecast for a period of sub-potential growth rather than an outright contraction. The factors that we expected would drag the economy into a recession remain; thus, we still expect a slow rate of expansion, and recession risk remains elevated. Our 2024 GDP outlook increased from a 0.3 percent Q4/Q4 contraction to a 1.1 percent Q4/Q4 increase.

Labor Market

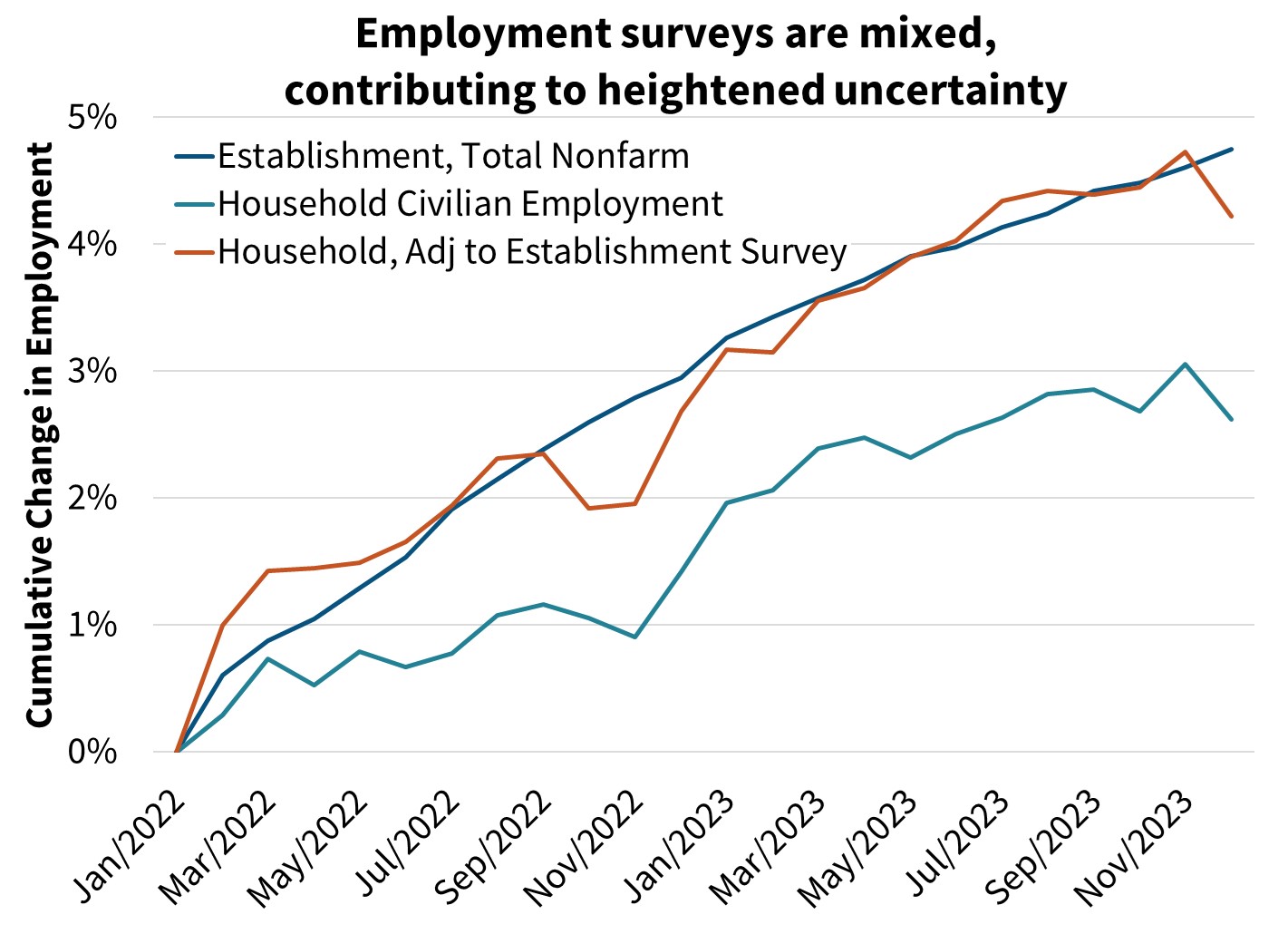

Compared to last month, our forecast unemployment rate was revised downward consistent with the removal of our recession call in 2024. We now expect a lesser and gradual move upward over the coming quarters corresponding to sub-trend economic growth, with the unemployment rate ending 2024 at 4.2 percent. Nonfarm payroll employment growth was 216,000 in December. The unemployment rate was unchanged at 3.7 percent.

Inflation & Monetary Policy

The December Consumer Price Index (CPI) report came out after the completion of our forecast and was slightly hotter than the market’s expectations. The headline Consumer Price Index grew 0.3 percent over the month and 3.4 percent compared to a year ago. Core inflation was more persistent, rising 0.3 percent over the month, but decelerating one-tenth to 3.9 percent on an annual basis. Our modest upward revision to our inflation forecast over our time horizon largely stems from the removal of our recession expectation, therefore lessening downward price pressures, especially on energy and other commodities prices.

Our baseline expectation is that the Fed will begin a series of interest rate cuts starting in May, totaling 100 basis points by end of the year. Given current financial market pricing implying greater easing, there is some upside risk to the total number of rate cuts in our forecast.

Housing & Mortgage Forecast Changes

Mortgage Rates

Following the Fed "pivot" in December, an anticipation of more dovish policy, and the recent decline in interest rates, our mortgage rate forecast has been revised meaningfully lower this month. We expect the FRM30 rate to average 6.1 percent in 2024 and 5.6 percent in 2025.

Existing Home Sales

Existing home sales came in largely as expected in November. Our forecast revision was driven largely by the lower projected interest rate environment and the removal of our recession call.

New Home Sales

New single-family home sales declined 12.2 percent to a seasonally adjusted annualized rate (SAAR) of 599,000 in November; however, this series is volatile. The lower projected interest rate path and the removal of our recession call led us to upgrade the forecast for new home sales for most of our forecast horizon, as was done with existing home sales. New home sales are historically more sensitive to economic downturns, so in changing our economic outlook, the forecast revision is proportionally large relative to the change in our existing home sales forecast.

Single-Family Housing Starts

Single-family housing starts jumped to a SAAR of 1.14 million, which we expect is not sustainable given incoming permits data, which tends to be a less volatile series, coming in at a lower pace of 977,000. While we expect a near-term pullback in the starts number, we have revised our forecast upward reflecting the lower projected interest rate path and the removal of our recession call. We continue to expect that the lack of existing homes available for sale will contribute to ongoing growth in new home construction.

Multifamily Housing Starts

Multifamily housing starts rose to a SAAR of 417,000, while permits fell to a SAAR of 490,000. We have slightly upgraded our near-term forecast based on this incoming data. Soft rent growth coupled with increasing supply deliveries is keeping our forecast for multifamily starts muted, but due to the revision to our interest rate and macroeconomic outlook, multifamily starts were also revised upward. However, we still project a decline of 18.3 percent in 2024 from 2023.

Single-Family Home Prices

Home prices grew 7.1 percent Q4/Q4 in 2023, according to the most recently published non-seasonally adjusted Fannie Mae Home Price Index, hotter than previously forecast. Overall, our home price growth forecast was revised upward through the forecast horizon, reflecting this recent momentum and revision to our interest rate and macroeconomic outlook from September to December.

")

Single-Family Mortgage Originations

We expect single-family purchase origination volumes to be $1.5 trillion in 2024, an upgrade of $49 billion, driven primarily by upgrades to the home sales and home price forecasts. We expect single-family purchase volumes to grow to $1.7 trillion in 2025, an upward revision of $67 billion from last month.

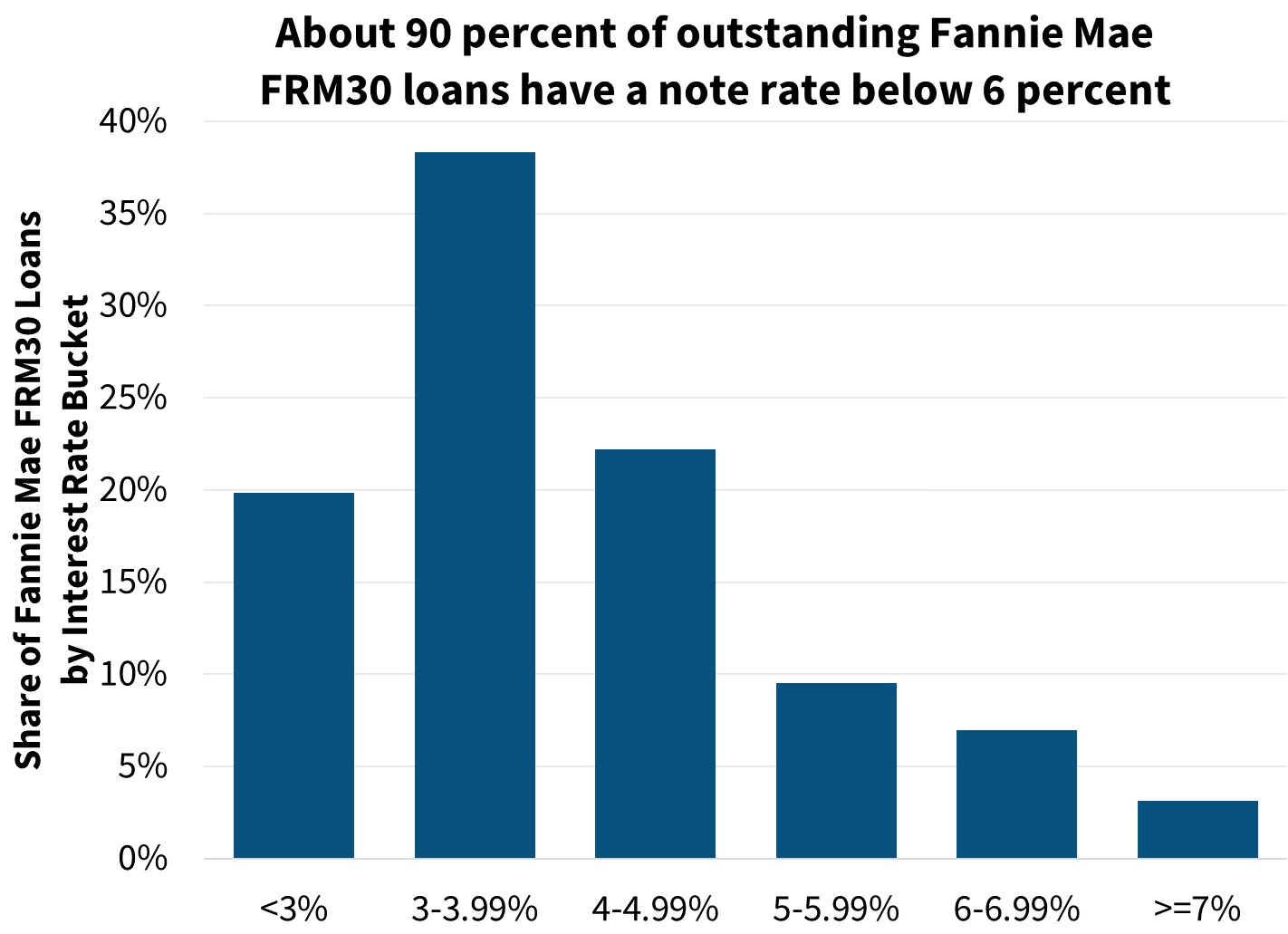

For single-family refinance originations, we project 2024 volumes will be $490 billion, an upgrade of $39 billion, driven by the lower mortgage rate forecast. Lately, we have observed a slight uptick in refinance application volume given rate decreases, as measured by Fannie Mae's Refinance Application Level Index (RALI). In 2025, we expect refinance volumes to grow to $752 billion.

Economic & Strategic Research (ESR) Group

January 12, 2024

For a snapshot of macroeconomic and housing data between the monthly forecasts, please read ESR's Economic and Housing Weekly Notes.

Data sources for charts: Bureau of Economic Analysis, Bureau of Labor Statistics, Census Bureau, National Association of REALTORS, Freddie Mac, Fannie Mae, Federal Reserve

Opinions, analyses, estimates, forecasts and other views of Fannie Mae's Economic & Strategic Research (ESR) Group included in these materials should not be construed as indicating Fannie Mae's business prospects or expected results, are based on a number of assumptions, and are subject to change without notice. How this information affects Fannie Mae will depend on many factors. Although the ESR group bases its opinions, analyses, estimates, forecasts and other views on information it considers reliable, it does not guarantee that the information provided in these materials is accurate, current or suitable for any particular purpose. Changes in the assumptions or the information underlying these views could produce materially different results. The analyses, opinions, estimates, forecasts and other views published by the ESR group represent the views of that group as of the date indicated and do not necessarily represent the views of Fannie Mae or its management.

ESR Macroeconomic Forecast Team

- Doug Duncan, SVP and Chief Economist

- Mark Palim, VP and Deputy Chief Economist

- Eric Brescia, Economics Manager

- Nick Embrey, Economics Manager

- Nathaniel Drake, Economic Analyst

- Richard Goyette, Economic Analyst

- Daniel Schoshinski, Economic Analyst

- Ryan Gavin, Economic Analyst