Economic Developments - February 2024

For a PDF version of this report, click here.

We continue to expect a modest recovery in home sales over the course of 2024 and for mortgage rates to drift downward. With recent home sales and mortgage application measures coming in near our expectations, we have made only modest adjustments to our housing outlook. We expect total home sales in 2024 to rise 5.0 percent to 5.00 million units, a slight upgrade from 4.96 million units in our prior forecast. We expect the 30-year fixed mortgage rate to decrease to 5.9 percent by the end of 2024, a tick higher than our prior outlook. Despite the slight upward revision to home sales, incoming mortgage application data, combined with an adjustment to the projected cash share of home sales, caused a modest downward revision to our forecast for mortgage originations. We forecast total mortgage origination volume will be $1.92 trillion in 2024 (compared with $1.98 trillion in our previous forecast) and $2.36 trillion in 2025 (compared with $2.44 trillion in our previous forecast).

Real Gross Domestic Product (GDP) was stronger in Q4 2023 than anticipated. As such, we have upgraded our 2024 GDP forecast largely due to stronger momentum to start the year. Additionally, primarily due to the brisk pace of immigration, we have revised upward our underlying assumptions on population and labor force growth, contributing to an upward revision to our GDP and employment forecasts. However, we still anticipate deceleration this year as consumer and local government spending growth slow and the continuing effects of tighter monetary policy work their way through the economy. However, if growth continues to surprise to the upside or inflation proves more persistent than anticipated, this would likely lead to upward pressure on mortgages rates as market participants adjust their fed funds rate cut expectations.

Economic Growth Remains Robust but Softening Still Anticipated

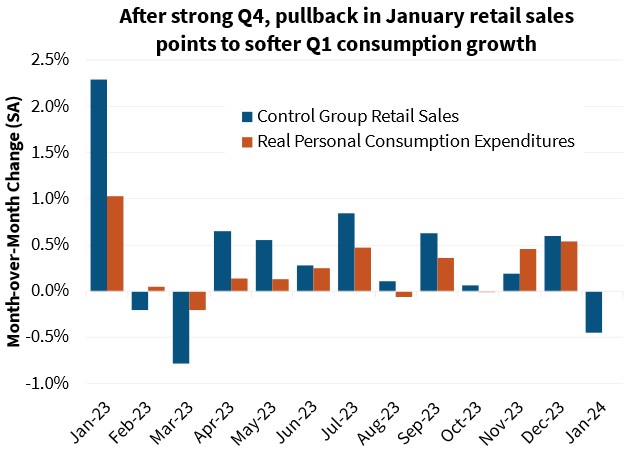

Still, we continue to anticipate growth will decelerate in 2024, albeit more modestly than previously forecast, due to both the lagged effects of higher interest rates weighing on business investment and an expected softening in components that drove strong fourth quarter growth. First, the saving rate moved down to just 3.7 percent in December, its lowest level in a year and roughly half its 2019 average. As such, we believe the surge in consumption in December is unsustainable and consumption growth will soften as the year progresses. Consistent with this expectation, January retail sales fell 0.8 percent over the month, which points to a pullback in consumer spending in the next release. While some of the retail sales softness was due to lower gasoline prices, most spending categories showed weakness, with the “core sales” that feed into the GDP estimates falling 0.4 percent. Furthermore, we expect some reversal in business inventory investment, and, with a weak global economic backdrop, we expect net exports to slow. Finally, state and local government tax receipts are softening, pointing to weaker future direct government spending growth.

Payroll employment surprised to the upside in January, increasing by 353,000, the strongest gain in a year. Following an upward revision of 117,000 jobs to December, nonfarm payroll growth over the past two months looks to have reaccelerated. In contrast, most other labor market measures point to softening. The alternative measure of household employment used to estimate the unemployment rate remains on a much weaker trend than the payroll survey. Additionally, the quits rate is slightly below the pre-pandemic rate, and the job openings rate continues to gradually decline. Broad measures of compensation growth, including the fourth quarter Employment Compensation Index (ECI) and the Atlanta Fed Wage Tracker, indicate that wage growth has also slowed. As such, we continue to expect slowing payroll growth as the year progresses and for the unemployment rate to gradually drift upwards.

Based on a reassessment of an assortment of population and immigration measures, we have upwardly revised our underlying projection of working-age population growth over our forecast horizon, driven primarily by the view of continued heightened net-immigration flows. While the trajectory of immigration going forward is heavily dependent on a mix of economic conditions and public policy decisions both here and abroad, we are setting as a baseline to our forecast a similar implied pace of net immigration through 2025 as was experienced in 2023. This led to a modest upward revision to our payroll and GDP forecasts, and if the trend is sustained, would imply a stronger pace of household formation and housing construction over the long run.

Existing home sales dipped slightly in December by one percent to a SAAR pace of 3.78 million units, the slowest pace since 2010. While this was a little lower than we had expected, more recent data on mortgage applications, as well as December pending homes sales, which lead closings on average by 30-45 days, show a modest rebound in sales is underway. Combined with a modest change in our mortgage rate forecast, we have made a moderate change to our existing home sales outlook.

The January 2024 Fannie Mae Home Purchase Sentiment Index® (HPSI) rose 3.5 points to 70.7, the strongest level since March 2022. Driving much of this change was the anticipation that mortgage rates will decline, as the survey reported the highest net share of consumers expecting mortgage rates to decline since its inception in 2011.

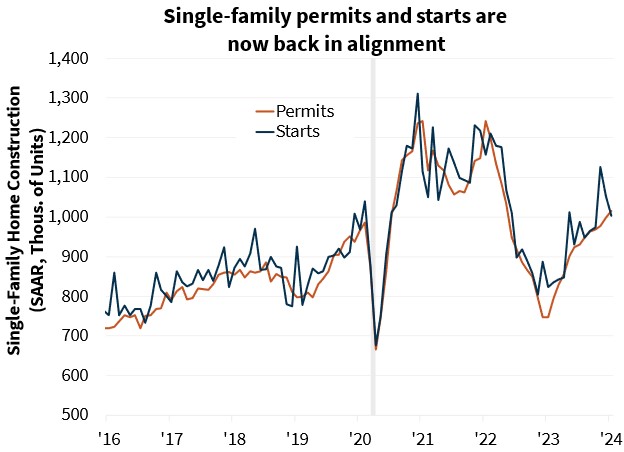

The pace of single-family housing starts fell in January; however, this was expected given the surge in November and the unseasonably warm weather in December. The pace of single-family starts had recently disconnected from the underlying housing permit series. Single-family permits in contrast edged up 1.6 percent in January, back in line with the overall starts series. With single-family permits and starts now back in alignment, we expect new single-family construction to continue to drift upward in coming months. With a low supply of existing homes for sale, demand for new homes is likely to remain strong, and the limit on new home sales will be determined by homebuilder production capacity.

Economic Forecast Changes

Economic Growth

The preliminary estimate for Q4 2023 GDP growth from the Bureau of Economic Analysis (BEA) showed that GDP grew at an annualized rate of 3.3 percent, above both the consensus expectation and our own. The bulk of the change from our prior forecast was driven by the new higher starting point in Q4 2023 and stronger consumption expectations. As a result, we’ve upwardly revised our GDP path, though we continue to expect growth to slow for some time to a rate below the long-run potential output trend. Therefore, our 2024 GDP outlook increased from a 1.1 percent Q4/Q4 increase to a 1.7 percent Q4/Q4 increase.

Labor Market

Nonfarm payroll employment growth was 353,000 in January. The unemployment rate was unchanged at 3.7 percent for the third consecutive month. Compared to last month, our forecasted unemployment rate was essentially unchanged; we continue to expect a gradual rise over the coming quarters, though we expect the unemployment rate to remain below the non-accelerating inflation rate of unemployment (better known as NAIRU) in 2024.

Inflation & Monetary Policy

The January Consumer Price Index (CPI) report came out after the completion of our forecast and was higher than the market’s expectation. Headline CPI grew 0.3 percent over the month and 3.1 percent compared to a year ago. Core inflation was more persistent, rising 0.4 percent over the month, with the annual rate unchanged at 3.9 percent, as a jump in shelter inflation offset a decline in used auto prices. The major change to our inflation expectations came from the lower oil price path, stronger assumed population growth leading to a less tight labor market, and a reassessment of core inflation less shelter; though, as the January CPI report shows, there is upside risk to our inflation expectations.

Our baseline expectation is that the Fed will maintain its current rate policy until June, when we expect the first rate cut.

Housing & Mortgage Forecast Changes

Mortgage Rates

Following the slight increase in interest rates in January, our interest rate forecast is slightly higher this month. We expect the 30-year fixed mortgage rate, as measured by Freddie Mac’s Primary Mortgage Market Survey (PMMS), to average 6.2 percent in 2024 and 5.7 percent in 2025. However, interest rates remain volatile, particularly given changes in Fed policy expectations, which adds risk to our outlook for interest rates.

Existing Home Sales

Existing home sales were at a SAAR of 3.78 million in December. We have revised our forecast modestly upward in 2024, mostly due to higher growth expectations, while we have lowered our expectations in 2025, largely due to the slightly higher projected interest rate environment. However, the continued heightened volatility of long-run interest rates continues to point to risk around the sales projection.

New Home Sales

New single-family home sales rose 8.0 percent to a SAAR of 664,000 in December. Similar to our existing home sales forecast, sales in 2024 were revised upward due to higher growth expectations, while sales in 2025 were revised downward slightly given the slightly higher projected interest rate path. New home sales continue to benefit from the limited inventory of existing homes for sale.

Single-Family Housing Starts

Single-family housing starts fell to a SAAR of 1.03 million in December, while permits rose to 999,000. The pullback was less than expected. Combined with a stronger growth outlook, we have revised our single-family starts forecast upward. We continue to expect that the lack of existing homes available for sale will continue to boost new home construction in the medium term.

Multifamily Housing Starts

Multifamily housing starts rose to a SAAR of 433,000 in December, while permits rose to a SAAR of 494,000. We have slightly upgraded our near-term forecast to reflect incoming data, but multifamily starts remain likely to decline as national rent growth has been muted and more multifamily units near completion.

Single-Family Home Prices

Home prices grew 7.1 percent Q4/Q4 in 2023, according to the most recently published non-seasonally adjusted Fannie Mae Home Price Index (HPI). Our next home price update will be in April.

")

Single-Family Mortgage Originations

We now expect 2024 single-family purchase origination volumes to be $1.5 trillion and 2025 volumes to be $1.6 trillion. These represent downgrades of $30 billion and $40 billion, respectively, compared to last month’s forecast. The downward revision to the 2024 forecast was driven by weaker-than-expected incoming data on the average price of new home sales. This outweighed upward revisions to our expectation for 2024 existing home sales.

For refinances, we have revised downward our overall volume expectation by $30 billion in 2024 to $459 billion, driven by the higher mortgage rate expectation this month. However, in the near term, we expect refinance volumes to continue to tick upward, consistent with recent readings from the Refinance Application Level Index (RALI). In 2025, we expect refinance volumes to grow to $709 billion, another downgrade from last month’s forecast driven by the change in our mortgage rate expectations.

Economic & Strategic Research (ESR) Group

February 16, 2024

For a snapshot of macroeconomic and housing data between the monthly forecasts, please read ESR's Economic and Housing Weekly Notes.

Data sources for charts: Bureau of Economic Analysis, Bureau of Labor Statistics, Census Bureau, National Association of REALTORS, Freddie Mac, Fannie Mae

Opinions, analyses, estimates, forecasts and other views of Fannie Mae's Economic & Strategic Research (ESR) Group included in these materials should not be construed as indicating Fannie Mae's business prospects or expected results, are based on a number of assumptions, and are subject to change without notice. How this information affects Fannie Mae will depend on many factors. Although the ESR group bases its opinions, analyses, estimates, forecasts and other views on information it considers reliable, it does not guarantee that the information provided in these materials is accurate, current or suitable for any particular purpose. Changes in the assumptions or the information underlying these views could produce materially different results. The analyses, opinions, estimates, forecasts and other views published by the ESR group represent the views of that group as of the date indicated and do not necessarily represent the views of Fannie Mae or its management.

ESR Macroeconomic Forecast Team

- Doug Duncan, SVP and Chief Economist

- Mark Palim, VP and Deputy Chief Economist

- Eric Brescia, Economics Manager

- Nick Embrey, Economics Manager

- Nathaniel Drake, Economic Analyst

- Richard Goyette, Economic Analyst

- Daniel Schoshinski, Economic Analyst

- Ryan Gavin, Economic Analyst