Mortgage Lenders' Demand Expectations for Purchase Mortgages Fall Significantly but Remain Stable and Strong for Refi

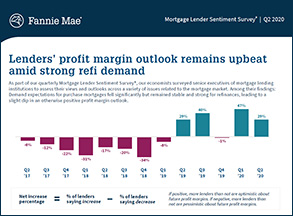

WASHINGTON, DC –Mortgage lenders' profit margin outlook for the next three months fell slightly but remained positive due to strong reported refinance demand, according to Fannie Mae's Q2 2020 Mortgage Lender Sentiment Survey®. This quarter, 52% of lenders believe profit margins will increase compared to the prior quarter, while 24% believe profits will remain the same and 23% believe profits will decrease. The increased optimism supplements prior quarter MLSS results revealing already-strong lender expectations of profitability. The survey of senior mortgage executives was conducted between May 5, 2020 and May 18, 2020.

Continuing strong consumer demand for refinance mortgages, in particular, outweighed a reported decline in purchase mortgage demand and drove lenders' expectations of increased profitability, with GSE pricing and policies cited by lenders as the second most common reason for the optimistic outlook. Interestingly, for the first time in survey history, more lenders responded that they believe the U.S. economy is on the wrong track, rather than on the right track. After years of remaining largely unchanged, this quarter the majority of lenders reported tightening credit standards across all loan types.

"This quarter's results reflect the impact of COVID-19 on all fronts," said Fannie Mae Senior Vice President and Chief Economist Doug Duncan. "Lenders' reported purchase mortgage demand for the prior three months and expectations for the next three months declined significantly from last quarter across all loan types. Demand for non-GSE eligible loans showed a sharper drop, reaching the lowest reading since survey inception, indicating a shift toward the GSE-eligible lending market. Lenders attributed the purchase mortgage demand decline to COVID-19-related factors, including home price uncertainty, higher unemployment, policy changes, and lower inventory. Lenders pointed to the same reasons for credit tightening."

"There are, however, encouraging signs," continued Duncan. "For the agency lending market, the purchase demand outlook remains positive on net and is well above the Q4 2018 reading, a period of accelerated declines. If borrowers perceive the bottom of the economic downturn as having passed, there could be a pickup in purchase demand to take advantage of continued low mortgage rates. Additionally, this quarter, refinance demand expectations held relatively stable, demonstrating continued strength. Lenders' profitability outlook remains positive, likely because of stable refinance demand, lender capacity constraints, and still-wide mortgage spreads. Nevertheless, challenges remain as the uncertainty around COVID-19 persists, in particular for mortgage servicing."

Mortgage Lender Sentiment Survey Highlights

Wide Mortgage Spreads Persist and Continue to Point to Positive Profitability Outlooks

Mortgage spreads remain elevated, consistent with mortgage lenders' profitability outlook. The average primary mortgage spreads (FRM 30 contract rate versus 10-year Treasury) came in at 256 basis points in May, above the long-run average of 168 basis points.

Purchase Mortgage Demand Fall Significantly; Refinance Mortgage Demand Holds Stable

For purchase mortgages, the net share of lenders reporting demand growth for both the prior three months and the next three months fell significantly from last quarter across all loan types (GSE-eligible, non-GSE-eligible, and government). For non-GSE-eligible mortgages, the net share reporting demand growth for both the prior three months and the next three months reached survey lows.

For refinance mortgages, the net share of lenders reporting demand growth over the prior three months remained strong, and reached a survey high for GSE-eligible loans. Demand growth expectations on net for the next three months fell from last quarter but remained high across all loan types.

Credit Standards Tightened

After years of stability, this quarter, the majority of lenders reported tightening credit standards. Across all loan types, the net share of lenders reporting easing credit standards for both the prior three months and the next three months significantly decreased, reaching survey lows.

About Fannie Mae's Mortgage Lender Sentiment Survey

The Mortgage Lender Sentiment Survey by Fannie Mae polls senior executives of its lending institution customers on a quarterly basis to assess their views and outlook across varied dimensions of the mortgage market. The Fannie Mae second quarter 2020 Mortgage Lender Sentiment Survey was conducted between May 5, 2020 and May 18, 2020 by PSB in coordination with Fannie Mae. For detailed findings from the second quarter 2020 survey, as well as survey questionnaires and other supporting documents, please visit the Fannie Mae Mortgage Lender Sentiment Survey page on fanniemae.com. Also available on the site are special topic analyses, which focus on findings and analyses of important industry topics.

About Fannie Mae

Fannie Mae helps make the 30-year fixed-rate mortgage and affordable rental housing possible for millions of Americans. We partner with lenders to create housing opportunities for families across the country. We are driving positive changes in housing finance to make the home buying process easier, while reducing costs and risk. To learn more, visit:

fanniemae.com | Twitter | Facebook | LinkedIn | Instagram | YouTube | Blog

Media Contact

Matthew Classick

202-752-3662

Fannie Mae Newsroom

https://www.fanniemae.com/news

Photo of Fannie Mae

https://www.fanniemae.com/resources/img/about-fm/fm-building.tif

Fannie Mae Resource Center

1-800-2FANNIE

###

Opinions, analyses, estimates, forecasts, and other views of Fannie Mae's Economic & Strategic Research (ESR) Group included in these materials should not be construed as indicating Fannie Mae's business prospects or expected results, are based on a number of assumptions, and are subject to change without notice. How this information affects Fannie Mae will depend on many factors. Although the ESR Group bases its opinions, analyses, estimates, forecasts, and other views on information it considers reliable, it does not guarantee that the information provided in these materials is accurate, current, or suitable for any particular purpose. Changes in the assumptions or the information underlying these views could produce materially different results. The analyses, opinions, estimates, forecasts, and other views published by the ESR Group represent the views of that group as of the date indicated and do not necessarily represent the views of Fannie Mae or its management.