Economic Developments October 2019

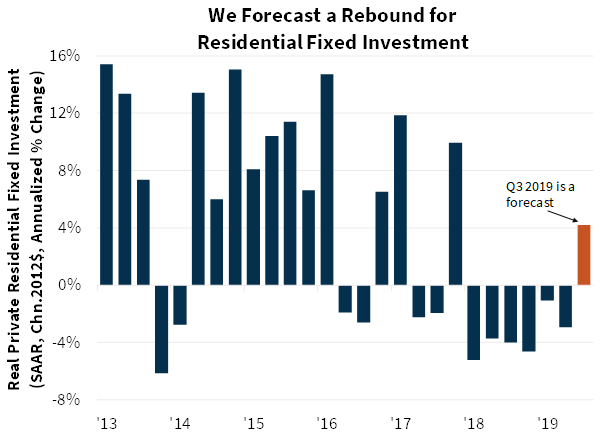

Third quarter 2019 residential fixed investment growth is expected to be positive for the first time since 2017. Increases in home sales, housing starts, and construction spending suggest housing will be supportive of growth, counteracting declining growth in business fixed investment and weak business inventory building. We revised downward our outlook on business investment and inventories in response to the General Motors shutdown, as well as the broader slowdown of the manufacturing sector, lowering our real gross domestic product (GDP) growth estimate for the third quarter by two-tenths to 1.7 percent annualized. The slowdown in growth will likely be temporary as we expect inventories to rebound and business investment to turn positive again in the final quarter of the year. Therefore, we maintained our top-line forecast for 2019 GDP growth at 2.2 percent. The GDP projection for 2020 rose one-tenth to 1.7 percent as we expect a still-solid labor market and gains in household wealth drive more consumer spending.

Our upward revision to 2020 U.S. GDP growth means a more positive outlook for housing. We expect total home sales in 2019 to increase by nearly 1.0 percent with another gain of about that magnitude in 2020. Housing starts were up across the forecast horizon with year-over-year growth expected in both 2019 and 2020, though they will remain below historical norms. The annual FHFA home price appreciation path was revised downward for 2019 as home price growth in recent months has been less sensitive to interest rate declines than previously expected, a signal that affordability constraints are still present in many markets. We continue to expect home price deceleration from 2019 but a persistently low interest rate environment likely means less slowdown than previously expected.

Trade tensions remain a key downside risk to our forecast. While the resumption of trade talks between the U.S. and China in early October seemed to offer some reprieve, tensions have since re-escalated as the U.S. administration blacklisted certain Chinese technology firms and imposed visa restrictions on some Chinese officials. Trade tensions have also flared between the U.S. and the European Union (EU) after the World Trade Organization approved U.S. tariffs on $7.5 billion of European goods. Trade uncertainty, weak European growth, and Brexit appear to be slowing global growth.

Our Call for Next Rate Cut Moves Forward

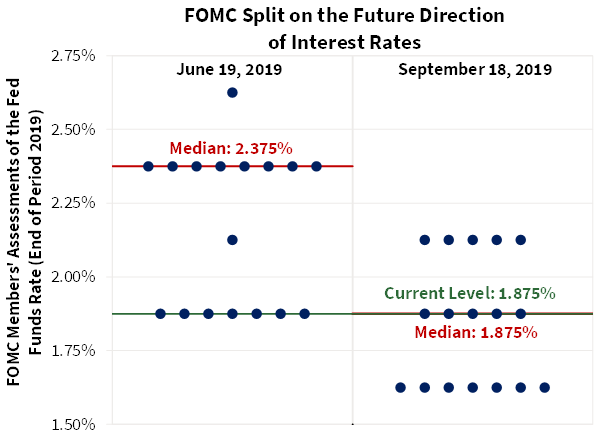

At its September meeting the Federal Open Market Committee (FOMC) lowered the federal funds rate by 25 basis points to a range of 1.75 percent to 2.00 percent, citing downside risks from trade policy uncertainty, the global growth slowdown, and adverse geopolitical developments. The dot plot, which shows the median forecast of the federal funds rate, indicated the median rate forecast for 2019 is now 1.875 percent, implying no more rate cuts this year, though there appears to be growing contention among participants about the best path forward, with seven members seeing an additional rate cut this year and five members believing the cut in September was a policy error. Despite the growing rifts among the committee, continued trade tensions, weak manufacturing, and the Fed's unwillingness to disappoint financial markets led us to move forward our forecast of 2019's final rate cut to October rather than December and include an additional cut in January of 2020 before pausing for the remainder of the year.

The September meeting minutes revealed another debate among committee members involved the Fed's forward guidance. Many members noted that financial markets expected more accommodation at coming meetings than the Fed believed was appropriate, and "that it might become necessary for the Committee to seek a better alignment of market expectations regarding the policy rate path." Indeed, a group of officials wanted the September post-meeting statement to provide clarity about when the central bank would end cutting interest rates in response to trade uncertainty.

The FOMC also directed cuts in the interest paid on excess reserves (IOER) and overnight reverse repurchase agreements amid tumult in the repurchase (repo) market, which saw rates jump as high as 10 percent in mid-Septmber due to reserve scarcity. The spike forced the central bank to conduct temporary operations for the first time in a decade, injecting liquidity into the market to pull rates down. While the initial lack of liquidity was due to technical factors, such as corporate tax payments and settlements of government bond sales, FOMC participants agreed in the September meeting minutes on the need to "discuss the appropriate level of reserve balances sufficient to support efficient and effective monetary policy." In mid-October the Fed announced it will purchase Treasury bills at least into the second quarter of 2020, allowing its balance sheet to grow "organically," buying only enough securities to maintain a level of reserve balances appropriate to facilitate policy instead of a large-scale asset-buying program intended to stimulate growth.

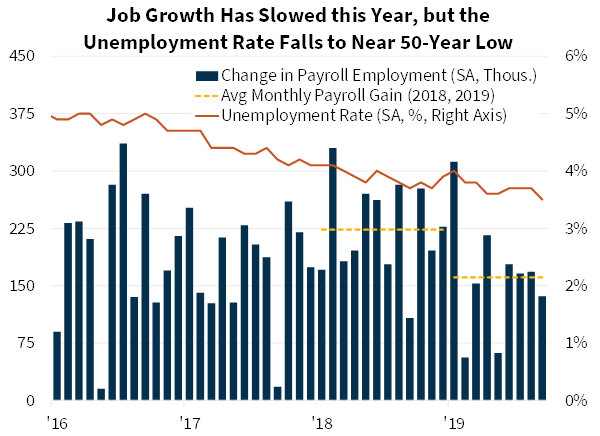

The labor market has done little to clarify divergent views among Fed officials as to whether the economy is slowing. Through September, monthly payroll growth in 2019 slowed to average 161,000 versus 223,000 in 2018; payroll gains have been strong enough, however, to pull down the unemployment rate to 3.5 percent, a 50-year low. The August Job Openings and Labor Turnover Survey (JOLTS) provided another sign of a slowing labor market, with job openings, an indicator of labor demand, continuing to trend downward and falling to the lowest level since March 2018. On a more positive note, while annual wage gains decelerated to the slowest pace this year for all private workers, wages for production and nonsupervisory workers fared better in September, rising 3.5 percent, close to the expansion best. We did not make substantive changes to our baseline view of employment this month, but we did alter our forecast to include temporary hiring for the upcoming decennial census. We believe that approximately 500,000 temporary workers will be hired over the next year with the bulk of the hiring taking place in the first and second quarter of 2020 before ending in the second half of next year. Finally, the ongoing strike of close to 50,000 General Motors (GM) employees represents another downside risk to the forecast. We expect that the strike will be resolved in the fourth quarter and therefore it had no visible impact on our employment forecast this month. However, if the strike and associated plant shutdowns drag on longer, our future forecasts will reflect negative spillovers that may force GM suppliers to lay off their own employees, resulting in a further drag to output and consumer spending.

Consumers Continue to Spend as Manufacturing Weakens Further

Real personal consumption expenditures (PCE) started off the third quarter strong, posting broad-based gains in July, before slowing in August to register the smallest increase since February. While we expect consumer spending to moderate significantly in the third quarter from the second quarter’s impressive 4.6 percent annualized pace, real disposable personal income posted the largest gain in six months in August, suggesting continued buying power at the end of the third quarter. We also revised up consumer spending throughout 2020 as we now believe solid labor market conditions will persist, wage growth will continue, and accommodative financial conditions will prevail. Consumer sentiment has remained highly resilient, though slightly less stable over the past several months. In September, two measures of consumer confidence were mixed with the Conference Board's measure recording the largest monthly decline this year, while the University of Michigan Index posted the largest gain in six months. We expect sentiment will remain highly volatile as consumers experience healthy income gains and a strong economy but continue to be buffeted by news of political tensions and trade uncertainties.

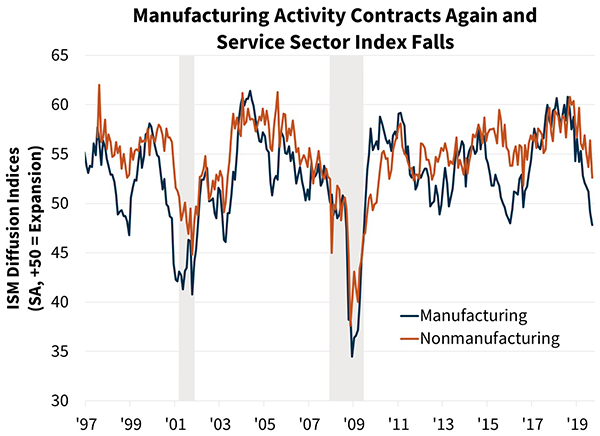

One risk to consumer spending in the coming quarters is weakness in business spending and manufacturing, which could eventually lead to slower hiring, in turn weighing on consumption. Surveys of purchasing managers from the Institute for Supply Management (ISM) showed that the manufacturing sector contracted in September for the second straight month, with the ISM manufacturing index falling to the lowest level of the expansion. Manufacturing employment declined in September and, combined with weak gains in the prior two months, in the third quarter posted the smallest gain in three years as firms seem to be exercising continuing caution in the face of global uncertainties. Additionally, while the ISM non-manufacturing index remained in its "expansion" range, it declined to the weakest level in three years. Weakness in business equipment investment is also obvious with the August factory orders report showing factory shipments declining to the lowest level in more than a year and factory orders falling for the first time in three months; moreover, both core shipments and core orders were revised lower from the advance estimates.

According to the Purchasing Managers' Index (PMI), global manufacturing contracted for the fifth straight month in September with significant weakness in the EU driven by declines in Germany and Italy. Trade tensions and an increasing shift towards protectionist policies have hit certain countries harder than others with economies highly exposed to trade, such as Germany, being more vulnerable to global economic slowdowns. Slower global growth has also been exacerbated by rising geopolitical uncertainties. Brexit is scheduled for the end of October, with the EU meeting for a final summit prior to that deadline next week. If the sides fail to reach a deal, it is likely the Brexit deadline will be extended for a third time to January 2020. Other geopolitical incidents include the protests in Hong Kong and the attacks on Saudi Arabia’s oil supplies, though oil production seems to have recovered quickly and has not been disrupted as much as was initially expected.

Lower Interest Rate Environment

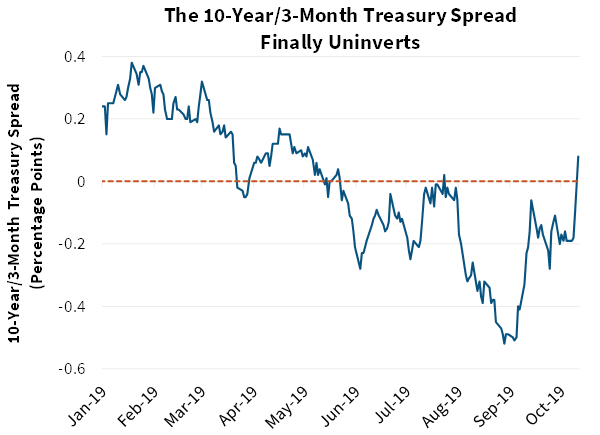

Interest rates were highly volatile in the third quarter. The 10-year yield began the third quarter at 2.03 percent before falling sharply to as low as 1.47 percent at the end of August and then rebounding slightly to end the quarter at 1.68 percent; the 10-year was 1.76 percent at the time of this writing. The 3-month yield has declined on the heels of rate cuts with the 10-year/3-month spread uninverting this week by the largest amount since May. At the longer end of the curve we have seen some stabilization in mortgage rates. The 30-year fixed mortgage rate averaged 3.61 percent in September, only 1 basis point under August’s monthly average but more than a full percentage point below year-ago levels.

In September, the primary spread (30-year mortgage rate minus 10-year yield) was 191 basis points versus a long-run average of around 170 basis points. This is consistent with lender capacity constraints and the Fed’s current policy of running off mortgage-backed securities from its balance sheet in favor of Treasuries. According to Fannie Mae's Mortgage Lender Sentiment Survey®, lender profitability sentiment hit a survey high in the third quarter even as credit standards shifted from net easing to net tightening. Lenders attributed their upbeat profitability outlook to consumer demand, particularly for refinance mortgages, driven by declining interest rates. As the 10-year stabilizes and lenders work through the higher volumes generated by a lower rate environment, we believe mortgage spreads will compress.

Housing Looks to Be on Solid Footing

While we had previously anticipated that housing activity would contribute positively to third quarter GDP, recent housing data have come in stronger than expected, leading us to revise upward our forecast for residential fixed investment to 4.2 percent annualized in the third quarter. We expect this strength to provide momentum into the fourth quarter, putting the remainder of the year on a solid footing. What had been a drag on the economy for almost two years will now likely be a near-term source of strength. While the effect has been somewhat modest relative to historical experience, lower interest rates are now clearly supporting the housing market.

Following a 2.5 percent jump in July, August existing single-family home sales pushed upward by 1.3 percent to 5.49 million annualized units, the strongest pace since March 2018. At the same time, new home sales rose 7.1 percent over the month to the second highest level since November 2017 and the third highest of the economic expansion. This recent strength led us to revise upward our third and fourth quarter home sales forecasts. We now expect total home sales in 2019 will be 0.9 percent higher than in 2018.

Home prices are also showing signs of strength. The CoreLogic National House Price index accelerated year over year in August after decelerating for fifteen of the past sixteen months. The July reading of the Case-Shiller house price index also came in roughly flat on an annual basis after a similar period of deceleration. While we still forecast slower house price growth for 2020 compared to 2019, lower interest rates and the associated growth in home sales have paused the strong slowdown in price growth expected this year.

The August decline in purchase mortgage applications and July's pending sales index still suggest a pullback in sales for September. The Fannie Mae Home Purchase Sentiment Index® pulled back slightly for the month as well, but we believe sales are likely to regain strength entering the fourth quarter. The August reading of the pending sales index, which leads sales by about 45 days on average, rose 1.6 percent, and purchase mortgage applications in September rebounded, rising 7.3 percent over the month.

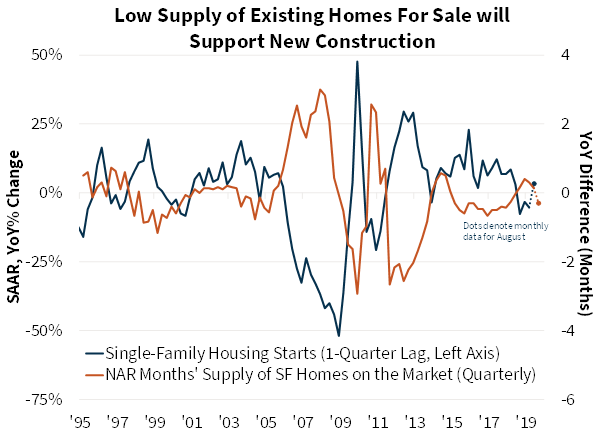

While we expect improvement in October, existing sales are likely near their peak pace for the time being, as the supply of homes for sale is not rising along with the sales pace. The months' supply of single-family homes for sale fell back to 4.0 months, the lowest August reading since the series began in 1982. Lower interest rates may still encourage additional homeowners to put their homes on the market as they no longer feel locked into their current mortgage rate, but there is little evidence of this occurring thus far. The continued shortage of homes for sale will persist as a limiting factor. We expect only a modest quarterly increase in fourth quarter existing home sales, and we project a modest softening moving into 2020 as economic growth is projected to decelerate while supplies remain tight.

The limited inventory of homes for sale should dampen existing sales but will likely be supportive of new construction. Total home sales are expected to increasingly rely on new construction to meet growing demand. Single-family housing starts rose for the third consecutive month in August to the second strongest pace since May 2018. While starts data can be volatile, the persistent increase in single-family housing permits suggests that new construction is indeed on an uptrend. Single-family permits jumped 5.5 percent in August to the highest level since February 2018. The Housing Market Index published by the National Association of Home Builders also continued to tick upward in September, indicating improving homebuilder sentiment. While homebuilders continue to face labor and land scarcity, holding back the potential pace of construction, the industry appears to have the capacity to maintain a comparatively heightened level of production. Strength in home building and stubbornly low inventories of existing homes for sale have led us to revise upward our forecast of single-family housing starts through next year.

Multifamily housing starts also jumped in August, surging 32.8 percent over the month, nearly reversing the declines of the prior two months. This series is volatile but, as with single-family construction, multifamily permits also jumped over the month. While we expect multifamily starts to cool somewhat over the upcoming quarters, the pace of construction is likely to remain quite strong in light of continued low vacancy rates, growing renter household formation, and low interest rates.

For more information on multifamily market conditions, please see the October 2019 Multifamily Market Commentary.

The upward revisions to our home sales forecast and 2020 home price path led to an increase in our forecast of purchase mortgage originations in 2019 and 2020 to $1.28 trillion and $1.29 trillion, respectively. Total originations for 2019 are expected to rise 15.4 percent from 2018 to $2.04 trillion. Looking ahead to 2020, we expect total originations to decline by 9.0 percent from this year to $1.86 trillion as projected declines in refinance activity outpace essentially flat purchase activity, with the refinance share dropping from 37 percent in 2019 to 31 percent in 2020.

Economic & Strategic Research (ESR) Group

(Data effective through October 11, 2019)

For a snapshot of macroeconomic and housing data between the monthly forecasts, please read ESR's Economic and Housing Weekly Notes.

Data source for charts: Federal Reserve, Bureau of Labor Statistics, Institute for Supply Management, Bureau of Economic Analysis, Census Bureau, National Association of REALTORS®, Fannie Mae ESR Group.

Opinions, analyses, estimates, forecasts and other views of Fannie Mae's Economic & Strategic Research (ESR) Group included in these materials should not be construed as indicating Fannie Mae's business prospects or expected results, are based on a number of assumptions, and are subject to change without notice. How this information affects Fannie Mae will depend on many factors. Although the ESR group bases its opinions, analyses, estimates, forecasts and other views on information it considers reliable, it does not guarantee that the information provided in these materials is accurate, current or suitable for any particular purpose. Changes in the assumptions or the information underlying these views could produce materially different results. The analyses, opinions, estimates, forecasts and other views published by the ESR group represent the views of that group as of the date indicated and do not necessarily represent the views of Fannie Mae or its management.

ESR Macroeconomic Forecast Team

- Doug Duncan, SVP and Chief Economist

- Brad Case, Director

- Rebecca Meeker, Financial Economist

- Nick Embrey, Economist

- Mark Palim, VP and Deputy Chief Economist

- Eric Brescia, Economist

- Richard Goyette, Business Analyst