Lenders Share Experiences with Front-End and Back-End Digital Transformation Investment

When investing in digital transformation1, more lenders say they focus on improving the front-end consumer experience than back-end operational efficiency, according to Fannie Mae's Mortgage Lender Sentiment Survey® (MLSS). Additionally, lenders reported a higher success rate with front-end digital transformation efforts than back-end efforts.

When investing in digital transformation1, more lenders say they focus on improving the front-end consumer experience than back-end operational efficiency, according to Fannie Mae's Mortgage Lender Sentiment Survey® (MLSS). Additionally, lenders reported a higher success rate with front-end digital transformation efforts than back-end efforts.

Digitization is rapidly changing how organizations create value and compete. Through previous studies, we found that lenders have consistently shown a strong interest in leveraging technology to improve both the front-end consumer experience and back-end operational efficiency.2 As part of the MLSS, we surveyed nearly 200 senior mortgage executives to better understand how lenders balance front- and back-end digital transformation investment, as well as how they assess the success of each.

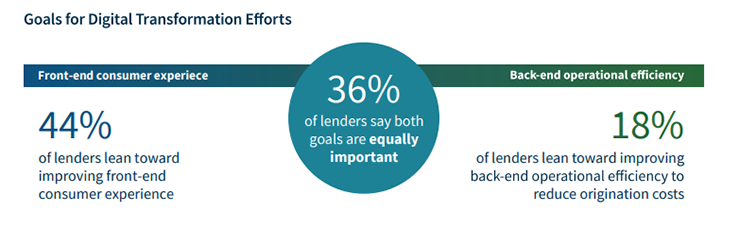

Forty-four percent of lenders indicated they tend to prioritize improving the front-end consumer experience, while 18 percent of lenders reported leaning toward improving back-end operational efficiency. Thirty-six percent of lenders gave approximately equal weight to each. When asked to assess the success of these efforts, more lenders view their front-end digital transformation efforts as having been more successful than their back-end efforts.

Lenders were also asked to identify the most important areas they focus on when improving the front-end borrower experience. Most lenders cited reducing cycle time, providing more user-friendly loan application platforms, and training personnel to be consultative as the most important focus areas. By contrast, reducing borrower costs was generally considered less important.

Lenders' responses indicate that they prefer to invest in front-end solutions, and they perceive them as more successful than back-end investments. Mortgage origination is complex – it involves many players in the value chain and many processes to transmit large volumes of data among a series of interconnected parties, including consumers, investors, and an array of service providers and stakeholders. Back-end operations are inherently more complicated than the front-end borrower experience. While most lenders cited the implementation of a Point-of-Sale (POS) system as a success example on the front-end, it is more difficult to implement a single solution to transform back-end operations.

Moreover, back-end digital transformation efforts face other roadblocks, including a talent shortage for digitizing legacy systems and less direct business case justification. While it's relatively straightforward to calculate returns on the implementation of a POS system, calculating returns on back-end digital transformation efforts is often more nebulous; and, any returns might stay negative for several years as these efforts generally do not yield immediate cost savings. Even so, continuous investment in robust and efficient back-end operations is critical to a well-functioning and sustainable mortage industry. These investments not only help to reduce human errors and rework but also translate fixed labor costs into variable costs, allowing a business to scale capacity up or down as the market expands or contracts.

To learn more, read our Fannie Mae Mortgage Lender Sentiment Survey Special Topic Report, "How Lenders Assess Their Digital Transformation Efforts."

Kimberly Johnson

Executive Vice President and Chief Operating Officer

October 16, 2019

The author thanks Steve Deggendorf and Li-Ning Huang for valuable contributions in the creation of this commentary and the design of the research. Of course, all errors and omissions remain the responsibility of the author.

Opinions, analyses, estimates, forecasts and other views reflected in this commentary should not be construed as indicating Fannie Mae's business prospects or expected results, are based on a number of assumptions, and are subject to change without notice. How this information affects Fannie Mae will depend on many factors. Changes in the assumptions or the information underlying these views could produce materially different results.

1 Digital transformation efforts could include, but are not limited to, implementing a Point-of-Sale system to streamline borrower mortgage applications, leveraging Application Programming Interfaces to transmit data, digitizing documents, and adopting newer technology solutions to streamline processes.

2 Examples include: "How Are Lenders' Business Priorities Evolving To Compete Against Industry Competition?" https://www.fanniemae.com/resources/file/research/mlss/pdf/lender-business-priorities-mlss-q22019.pdf

"APIs and Mortgage Lending," https://www.fanniemae.com/resources/file/research/mlss/pdf/apis-mortgage-lending-q12019.pdf

"How Will Artificial Intelligence Shape Mortgage Lending?" https://www.fanniemae.com/resources/file/research/mlss/pdf/mlss-artificial-intelligence-100418.pdf

Full Page Infographic

MLSS Special Topic Report