Desktop Underwriter update helps lenders better serve creditworthy borrowers

Fannie Mae is continuously innovating to improve the overall mortgage experience. Desktop Underwriter® (DU®) is one of several innovative solutions that reflect our commitment to delivering a simpler and more certain experience to our lenders and their customers. The DU platform leverages data and advanced analytics to generate recommendations that mitigate risk for lenders and investors while responsibly expanding homeownership opportunities.

Fannie Mae is continuously innovating to improve the overall mortgage experience. Desktop Underwriter® (DU®) is one of several innovative solutions that reflect our commitment to delivering a simpler and more certain experience to our lenders and their customers. The DU platform leverages data and advanced analytics to generate recommendations that mitigate risk for lenders and investors while responsibly expanding homeownership opportunities.

We have announced an update to Desktop Underwriter effective at the end of July that will enable our customers to better serve creditworthy borrowers. Specifically, the update will allow more loans with debt-to-income (DTI) ratios between 45 and 50 percent to receive a DU Approve/Eligible recommendation.

Updates to DU are carefully considered and influenced by over two decades of automated underwriting and experience with millions of mortgage loans – including many with high DTI ratios. This enables loan-level risk analysis based on a comprehensive set of criteria that reflects the complexity of predicting whether borrowers will repay their loans. To better understand the impact of the comprehensive criteria, it is important to consider the relationships among factors versus any one factor.

Debt-to-Income (DTI) ratio in context

The DTI ratio is a mainstay of mortgage loan underwriting. Desktop Underwriter considers DTI ratio as one factor, among many, in performing a comprehensive loan-level risk assessment. Fannie Mae regularly monitors and fine-tunes the DU risk model, with careful consideration given to “risk layering.” We define risk layering as combining multiple risk factors on a particular loan.

The maximum DTI ratio DU will accept on a specific loan depends on DU’s evaluation of the overall loan file, including risk layering analysis. For example, we allow as little as a 3 percent down payment, credit scores as low as 620, and credit for borrowers without credit scores who can document nontraditional credit histories. We can offer these and other flexibilities with DU because it assesses and manages the risk layers on a single loan.

Expected outcomes

We expect the DU update will result in more loans with DTI ratios between 45 and 50 percent receiving an Approve/Eligible recommendation from DU: approximately three to four percent of recent applications did not receive an Approve/Eligible recommendation but would receive one in DU 10.1 with these changes. That means they are eligible for sale and delivery to Fannie Mae (subject to any identified conditions on the loan-level DU Findings Report).

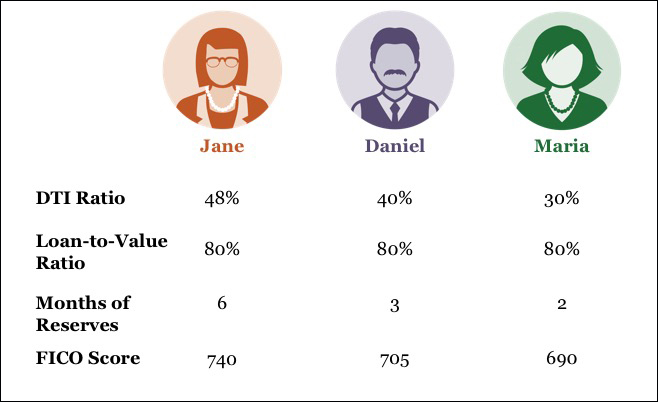

To illustrate the potential impact of the updated risk assessment, consider this example of three illustrative loans that present roughly equivalent risk – all three borrowers are buying a 1-unit principal residence at the same price using a 30-year fixed-rate mortgage. They have the same monthly income but their debts vary, so their DTI ratios also vary, along with their months of available reserves and credit profiles:

All three of these illustrative loans would receive a DU Approve/Eligible recommendation in DU 10.1. But note that Jane, with the highest DTI ratio at 48%, also has a stronger credit history and the most reserves.

Here are some key things to know:

- Under limited circumstances, we have been acquiring loans in the past four years with DTI ratios up to 50 percent, and that maximum is not changing.

- Borrowers with high DTI ratios must have a strong credit history to get a DU Approve/Eligible recommendation. DU’s analysis of credit report data, for example, looks favorably on a track record of repaying installment debts and revolving credit on time, with few or no delinquencies or defaults (for details, see the DU Credit Report Analysis).

- A maximum 50 percent DTI ratio as part of a comprehensive risk evaluation aligns with other investors in the industry. The DU risk evaluation considers a number of factors including credit history, equity and LTV ratio, liquid reserves, and loan purpose and term (view Risk Factors Evaluated by DU in the Selling Guide).

- This change aligns with our longstanding commitment to affordable lending and sustainable homeownership for creditworthy borrowers.

Other DU updates effective in July

Also with the release of DU Version 10.1, lenders and borrowers will benefit from several other policy simplifications:

- Maximum loan-to-value ratios for adjustable-rate and fixed-rate mortgages aligned at 95 percent.

- Less tax return income documentation to be required for many self-employed borrowers.

- Simplified approach to handling disputed tradelines.

Summary

DU’s evaluation is fair and objective, applying the same criteria to every mortgage application it considers. The DTI change and the other updates in DU Version 10.1 leverage the power of DU to make it even easier for lenders to expand homeownership opportunities.

Jude Landis

Vice President, Credit Policy

July 11, 2017

Business Partners

Homebuyers, Owners, & Renters

- Educational Resources

- Credit Basics

- HomeView Homeownership Education Course

- HomePath - Search for Homes

- Make Your Rent Count